Cxense ASA-Q1-2015-presentation - Jørgen Loeng

28

Cxense ASA Q1 2015 presentation 13 May 2015

-

Upload

cxense -

Category

Investor Relations

-

view

168 -

download

4

Transcript of Cxense ASA-Q1-2015-presentation - Jørgen Loeng

Cxense ASA Q1 2015 presentation 13 May 2015

2

THIS PRESENTATION AND ITS ENCLOSURES AND APPENDICES (HEREINAFTER JOINTLY REFERRED TO AS THE “PRESENTATION”) HAVE BEEN PREPARED BY CXENSE ASA (THE”COMPANY”) EXCLUSIVELY FOR INFORMATION PURPOSES. THIS PRESENTATION HAS NOT BEEN REVIEWED OR REGISTERED WITH ANY PUBLIC AUTHORITY OR STOCK EXCHANGE. RECIPIENTS OF THIS PRESENTATION MAY NOT REPRODUCE, REDISTRIBUTE OR PASS ON, IN WHOLE OR IN PART, THE PRESENTATION TO ANY OTHER PERSON. THE CONTENTS OF THIS PRESENTATION ARE NOT TO BE CONSTRUED AS LEGAL, BUSINESS, INVESTMENT OR TAX ADVICE. EACH RECIPIENT SHOULD CONSULT WITH ITS OWN LEGAL, BUSINESS, INVESTMENT AND TAX ADVISER AS TO LEGAL, BUSINESS, INVESTMENT AND TAX ADVICE. THERE MAY HAVE BEEN CHANGES IN MATTERS, WHICH AFFECT THE COMPANY SUBSEQUENT TO THE DATE OF THIS PRESENTATION. NEITHER THE ISSUE NOR DELIVERY OF THIS PRESENTATION SHALL UNDER ANY CIRCUMSTANCE CREATE ANY IMPLICATION THAT THE INFORMATION CONTAINED HEREIN IS CORRECT AS OF ANY TIME SUBSEQUENT TO THE DATE HEREOF OR THAT THE AFFAIRS OF THE COMPANY HAVE NOT SINCE CHANGED, AND THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE OR CORRECT ANY INFORMATION INCLUDED IN THIS PRESENTATION. THIS PRESENTATION INCLUDES AND IS BASED ON, AMONG OTHER THINGS, FORWARD-LOOKING INFORMATION AND STATEMENTS. SUCH FORWARD-LOOKING INFORMATION AND STATEMENTS ARE BASED ON THE CURRENT EXPECTATIONS, ESTIMATES AND PROJECTIONS OF THE COMPANY OR ASSUMPTIONS BASED ON INFORMATION AVAILABLE TO THE COMPANY. SUCH FORWARD-LOOKING INFORMATION AND STATEMENTS REFLECT CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS, UNCERTAINTIES AND ASSUMPTIONS. THE COMPANY CANNOT GIVE ANY ASSURANCE AS TO THE CORRECTNESS OF SUCH INFORMATION AND STATEMENTS. AN INVESTMENT IN THE COMPANY INVOLVES RISK, AND SEVERAL FACTORS COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE COMPANY TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS THAT MAY BE EXPRESSED OR IMPLIED BY STATEMENTS AND INFORMATION IN THIS PRESENTATION, INCLUDING, AMONG OTHERS, RISKS OR UNCERTAINTIES ASSOCIATED WITH THE COMPANY’S BUSINESS, SEGMENTS, DEVELOPMENT, GROWTH MANAGEMENT, FINANCING, MARKET ACCEPTANCE AND RELATIONS WITH CUSTOMERS, AND, MORE GENERALLY, GENERAL ECONOMIC AND BUSINESS CONDITIONS, CHANGES IN DOMESTIC AND FOREIGN LAWS AND REGULATIONS, TAXES, CHANGES IN COMPETITION AND PRICING ENVIRONMENTS, FLUCTUATIONS IN CURRENCY EXCHANGE RATES AND INTEREST RATES AND OTHER FACTORS. SHOULD ONE OR MORE OF THESE RISKS OR UNCERTAINTIES MATERIALISE, OR SHOULD UNDERLYING ASSUMPTIONS PROVE INCORRECT, ACTUAL RESULTS MAY VARY MATERIALLY FROM THOSE DESCRIBED IN THIS DOCUMENT. THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE OR CORRECT THE INFORMATION INCLUDED IN THIS PRESENTATION. THIS PRESENTATION IS SUBJECT TO NORWEGIAN LAW, AND ANY DISPUTE ARISING IN RESPECT OF THIS PRESENTATION IS SUBJECT TO THE EXCLUSIVE JURISDICTION OF NORWEGIAN COURTS

Important notice

3

We enable businesses to understand, engage and monetize their audience

• Real-time user tracking and profile building regardless of whether the users access the sites via mobile, tablet or desktop

• Individually tailored web content and advertisements create unique user experiences

• Proprietary «big data» management software

Attractive outlook and leading position

• Increasing focus on user-targeted marketing

• Still in early stages of adoption

Long-term client relationships

• Attractive business model

We enable businesses to understand, engage and monetize their audience

• Real-time user tracking and profile building regardless of whether the users access the sites via mobile, tablet or desktop

• Individually tailored web content and advertisements create unique user experiences

• Proprietary «big data» management software

Attractive outlook and leading position

• Increasing focus on user-targeted marketing

• Still in early stages of adoption

Long-term client relationships

• Attractive business model

Adopted by global media leaders Adopted by global media leaders

Cxense at a glance

SaaS revenues and gross margin

SaaS revenues and gross margin

50%

60%

70%

80%

90%

0

1 000

2 000

3 000

4 000

4Q12 1Q13 2Q13 3Q13 4Q13* 1Q14 2Q14 3Q14 4Q14 1Q15

USD

1 0

00

Revenues Gross margin

* Emediate included in revenues from 4Q13

4

Predictable high-growth revenue stream

The “SaaS” (software as-a-service) revenue model provides revenue visibility

12-24 month contract durations and auto renewal

Unique technology with infinite scalability and real-time accessibility

The Cxense data engine is a core part of our clients’ internet offering

More than half a billion user profiles maintained across more than 5 000 internet sites

Robust growth in several geographical markets and verticals

Powering premium publishers and E-commerce companies

The enterprise market has untapped potential

Market penetration accelerated with recent strengthening of sales team

Predictable high-growth revenue stream

The “SaaS” (software as-a-service) revenue model provides revenue visibility

12-24 month contract durations and auto renewal

Unique technology with infinite scalability and real-time accessibility

The Cxense data engine is a core part of our clients’ internet offering

More than half a billion user profiles maintained across more than 5 000 internet sites

Robust growth in several geographical markets and verticals

Powering premium publishers and E-commerce companies

The enterprise market has untapped potential

Market penetration accelerated with recent strengthening of sales team

Estimated annualized revenue from SaaS backlog at qtr. end

Estimated annualized revenue from SaaS backlog at qtr. end

SaaS is the business model for the future

Number of new contracts signed

Number of new contracts signed

10

11

12

13

14

15

16

17

18

19

2Q14 3Q14 4Q14 1Q15

US

Dm

0

5

10

15

20

25

30

35

40

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

5

Agenda

Highlights

Operational review

Financial review

Technology update

6

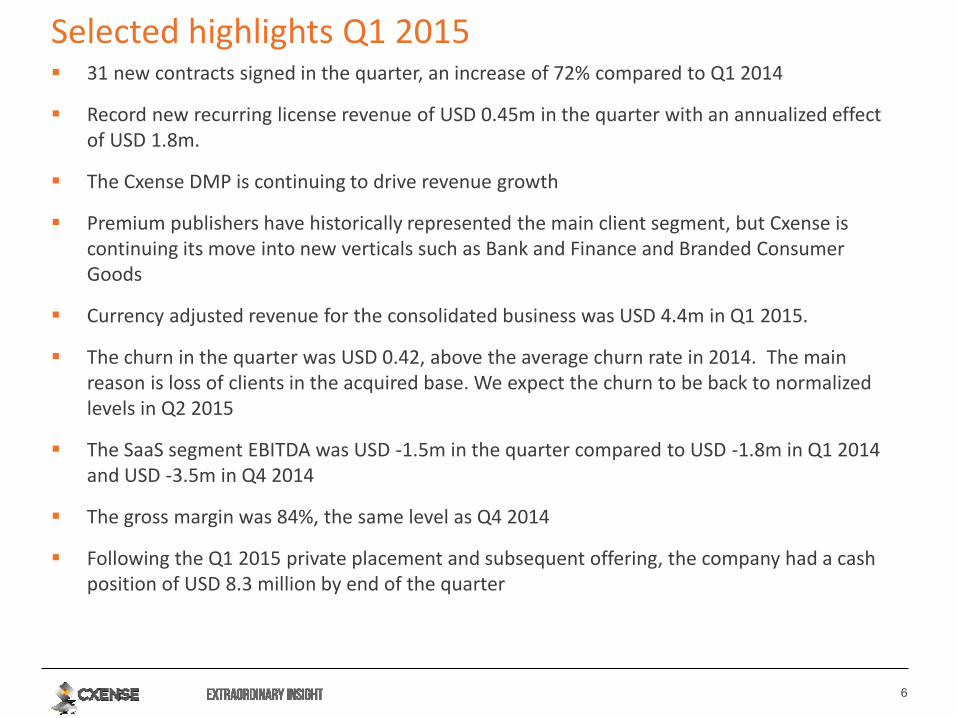

Selected highlights Q1 2015 31 new contracts signed in the quarter, an increase of 72% compared to Q1 2014

Record new recurring license revenue of USD 0.45m in the quarter with an annualized effect of USD 1.8m.

The Cxense DMP is continuing to drive revenue growth

Premium publishers have historically represented the main client segment, but Cxense is continuing its move into new verticals such as Bank and Finance and Branded Consumer Goods

Currency adjusted revenue for the consolidated business was USD 4.4m in Q1 2015.

The churn in the quarter was USD 0.42, above the average churn rate in 2014. The main reason is loss of clients in the acquired base. We expect the churn to be back to normalized levels in Q2 2015

The SaaS segment EBITDA was USD -1.5m in the quarter compared to USD -1.8m in Q1 2014 and USD -3.5m in Q4 2014

The gross margin was 84%, the same level as Q4 2014

Following the Q1 2015 private placement and subsequent offering, the company had a cash position of USD 8.3 million by end of the quarter

7

Agenda

Highlights

Operational review

Financial review

Technology update

8

EMEA Swedish Publisher

EMEA Spanish Publisher

Japan Japanese Publisher

North America Reseller/Partner

Latin America Broadcaster in South America

Selected contracts in Q1 2015

9

Strong momentum in new contracts and new recurring revenue

31 new contracts signed in the quarter. Slightly down from the record level in Q4 2014, but significantly above the average level for 2014, and a 71% increase compared to Q1 2014

The new recurring revenue is mainly from our DMP offering, where as last year it was mainly ad serving software

2015 new recurring revenue will continue to be dominated by the DMP offering

Cxense ASA has experienced an increasing number of invitations to RFP´s in North America and EMEA, both within publishing but also within the enterprise market

We are also experiencing also an increase in the number of companies approaching us for partner agreements

10

Business as usual for portfolio

We experienced higher churn in Q1 2015 – one lost contract represent a large part of total churn in Q1

The churn is from our acquired customer base (Q4 2013)

We expect the churn, in percentage of client base, to be the same for 2015 as for 2014

Quarterly churn in USD

11

2 20 5

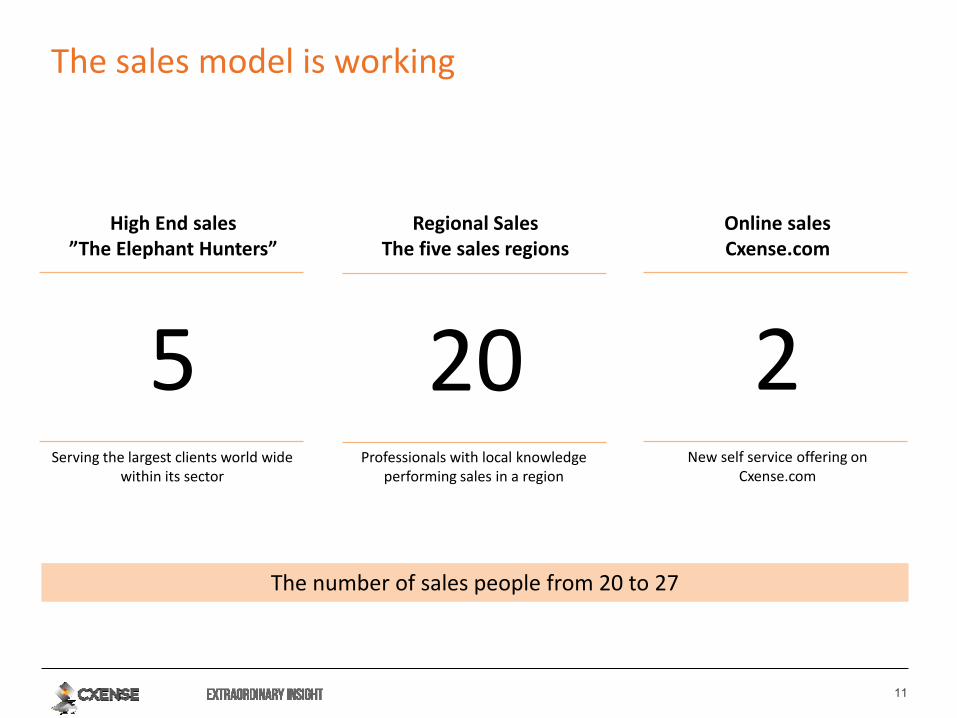

The sales model is working

High End sales ”The Elephant Hunters”

Regional Sales The five sales regions

Online sales Cxense.com

Serving the largest clients world wide within its sector

Professionals with local knowledge performing sales in a region

New self service offering on Cxense.com

The number of sales people from 20 to 27

12

Agenda

Highlights

Operational review

Financial review

Technology update

13

USD appreciation masks growing underlying SaaS sales

1.0

0.5

0.0

4.0

3.5

3.0

2.5

2.0

1.5

-8%

Q1 ’15

3.30

Q4 ’14

3.59

Q3 ’14

3.53

Q2 ’14

3.44

Q1 ’14

3.57

Reported SaaS segment revenues – USD million

0

4

8

12

16

20

24

2825.3

Q3 ’14

22.3

Q2 ’14

21.1

Q1 ’14

21.8

+19%

Q4 ’14 Q1 ’15

25.9

SaaS segment revenues – NOK million*

*Calculated from reported revenues using average quarterly FX rates

14

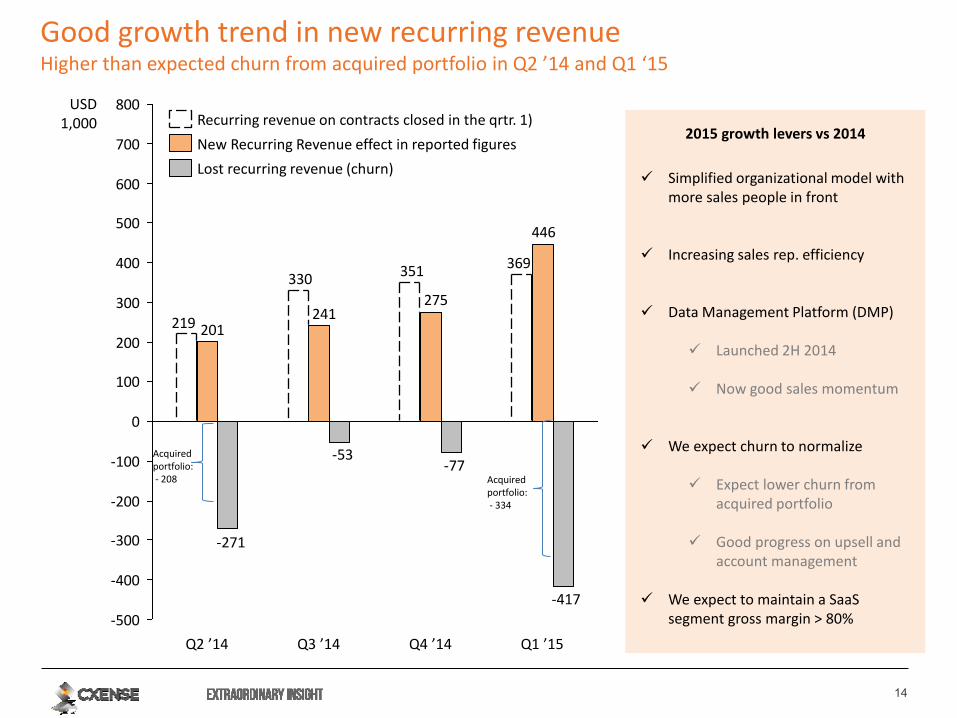

Good growth trend in new recurring revenue Higher than expected churn from acquired portfolio in Q2 ’14 and Q1 ‘15

369351330

219

446

275241

201

-417

-77-53

-271

-500

-400

-300

-200

-100

0

100

200

300

400

500

600

700

800

Q3 ’14 Q2 ’14

USD 1,000

Q4 ’14 Q1 ’15

Recurring revenue on contracts closed in the qrtr. 1)

Lost recurring revenue (churn)

New Recurring Revenue effect in reported figures

Acquired portfolio: - 334

Acquired portfolio: - 208

2015 growth levers vs 2014

Simplified organizational model with more sales people in front

Increasing sales rep. efficiency

Data Management Platform (DMP)

Launched 2H 2014

Now good sales momentum

We expect churn to normalize

Expect lower churn from acquired portfolio

Good progress on upsell and account management

We expect to maintain a SaaS segment gross margin > 80%

15

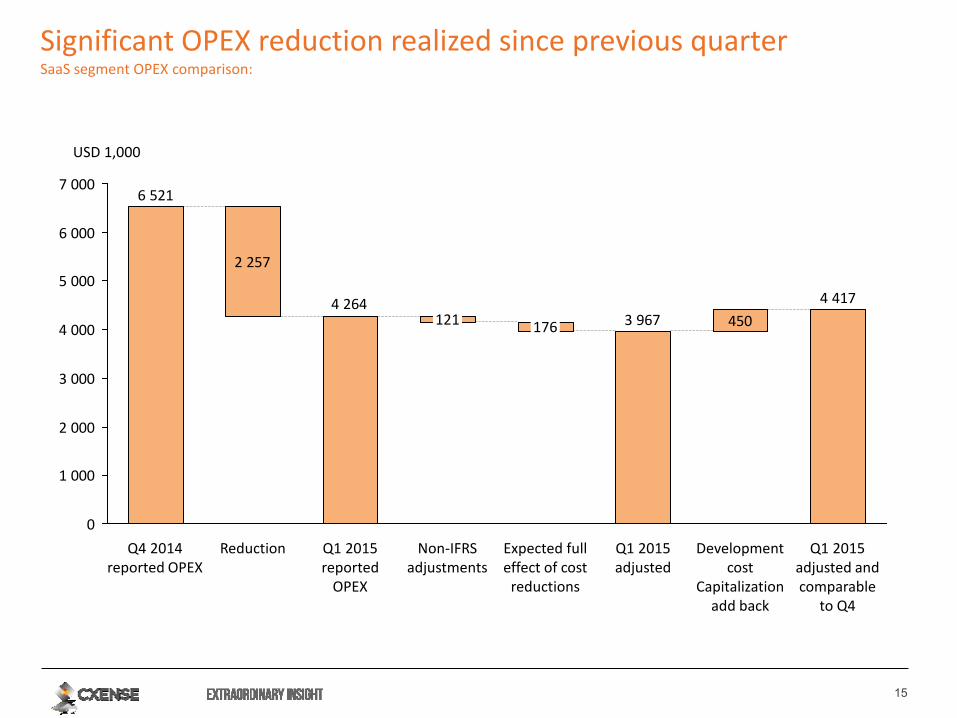

Significant OPEX reduction realized since previous quarter SaaS segment OPEX comparison:

2 257

4 417

4504 264

6 521

3 967

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Q1 2015 reported

OPEX

Reduction Q4 2014 reported OPEX

176

Expected full effect of cost

reductions

Q1 2015 adjusted

121

Non-IFRS adjustments

Q1 2015 adjusted and comparable

to Q4

Development cost

Capitalization add back

USD 1,000

16

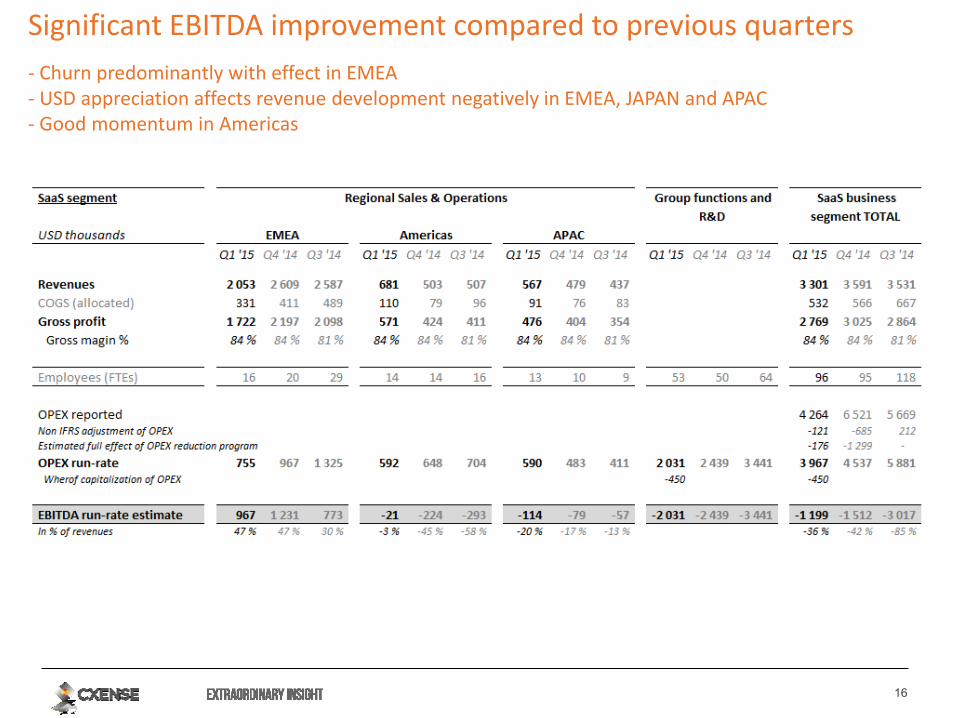

Significant EBITDA improvement compared to previous quarters x

- Churn predominantly with effect in EMEA - USD appreciation affects revenue development negatively in EMEA, JAPAN and APAC - Good momentum in Americas

17

Revenues

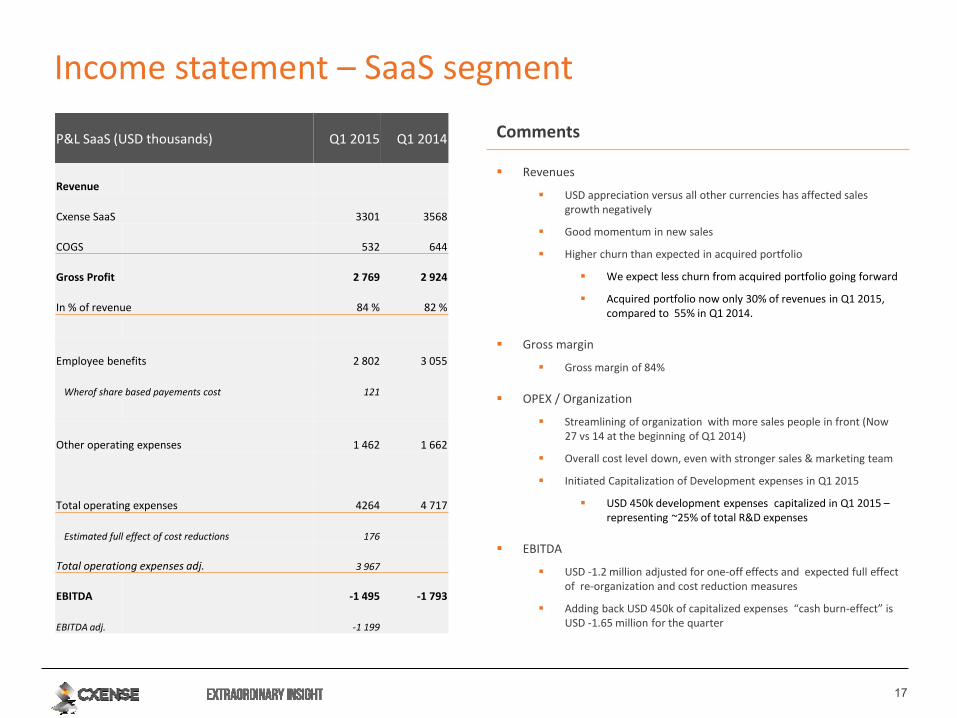

USD appreciation versus all other currencies has affected sales growth negatively

Good momentum in new sales

Higher churn than expected in acquired portfolio

We expect less churn from acquired portfolio going forward

Acquired portfolio now only 30% of revenues in Q1 2015, compared to 55% in Q1 2014.

Gross margin

Gross margin of 84%

OPEX / Organization

Streamlining of organization with more sales people in front (Now 27 vs 14 at the beginning of Q1 2014)

Overall cost level down, even with stronger sales & marketing team

Initiated Capitalization of Development expenses in Q1 2015

USD 450k development expenses capitalized in Q1 2015 – representing ~25% of total R&D expenses

EBITDA

USD -1.2 million adjusted for one-off effects and expected full effect of re-organization and cost reduction measures

Adding back USD 450k of capitalized expenses “cash burn-effect” is USD -1.65 million for the quarter

Income statement – SaaS segment

Comments P&L SaaS (USD thousands) Q1 2015 Q1 2014

Revenue

Cxense SaaS 3301 3568

COGS 532 644

Gross Profit 2 769 2 924

In % of revenue 84 % 82 %

Employee benefits 2 802 3 055

Wherof share based payements cost 121

Other operating expenses 1 462 1 662

Total operating expenses 4264 4 717

Estimated full effect of cost reductions 176

Total operationg expenses adj. 3 967

EBITDA -1 495 -1 793

EBITDA adj. -1 199

18

Consolidated Statement of Financial Position

Comments

Total assets of USD 20.9 million

Largest components:

Cash

Goodwill and intangible non-current assets related to the acquisition of Emediate and capitalized development costs.

Very limited fixed assets except for USD 400 thousand invested in hosting equipment under Office machinery, equipment etc.

Q4 2014 Trade receivables of USD 2.12 million (49 days) compared to USD 2.9 million (59 days) in Q4 2013.

Cash and cash equivalents of USD 8.3 million

Other short term assets of USD 1.6 million [including escrow account related to Emediate acquisition of ~USD 1 million]

Current liabilities of USD 4.8 million [including escrow account related to Emediate acquisition of ~USD 1 million]

Total equity of USD 15.6 million

USD thousands As of 31

Mar 2015 As of 31

Mar 2014

Non-current assets

Goodwill 3 807 3 807

Deferred tax assets 34 49

Intangible assets 4 434 5 337

Office machinery, equipment, etc. 400 279

Other financial assets 173 48

Total non-current assets 8 847 9 519

Current assets

Trade receivables 2 120 2 931

Other short-term assets 1 641 2 332

Cash and cash equivalents 8 291 5 936

Total current assets 12 051 11 199

Assets classified as "held for sale" 0 0

Total Assets 20 898 20 718

Total Equity 15 616 15 135

Non-current liabilities

Deferred tax liabilities 507 633

Total non-current liabilities 507 633

Non-current liabilities

Trade payables 1 100 1 112

Current taxes 77 58

Other short-term liabilities 3 597 3 780

Total current liabilities 4 775 4 950

Liabilities related to assets "held for sale" 0 0

Total equity and liabilities 20 898 20 718

19

Cash flow statement

Comments

• Net cash flow used in operating activities was USD 2.76 million in Q1 2015, compared to USD 2.86 million in Q1 2015 and USD 2.26 in Q4 2014.

• In Q1 2015 cash flow used in operating activities was significantly higher than the Q1 2015 EBITDA. This is explained by: – Significant accrued costs and trade payables at the end of

Q4 2014 that were paid during Q1 2015.

• The accrued costs in Q4 2014 relate mostly to the organizational streamlining done in Q4 2014 were provisions were made for costs with later payments following lay-offs.

– Currency translation effects also affected the Q1 2015 cash flow from operations negatively.

• In Q4 2014 we saw the opposite effect where cash flow from operations was significantly better than reported EBITDA.

• Investments in intangible assets in Q1 2015 relates to the cash effect of capitalized development expenses

*After the share issue there were 3 681 717 shares outstanding. There were also 718 634 warrants and 173 380 share options outstanding

Cash flow statement Q1 2015 Q1 2014

Cash flow from operating activities

P/(L) before income tax (inc. disposal group) -1 890 -2 147

Adjustments:

Income tax payable 29 -

Share- based payments 121 74

Result from investment in associates - -

Depreciation and amortization 358 313

Currency translation effects -624 117

Change in trade receivables 30 69

Change in trade payables -354 -821

Change in other accrual and non-current items -431 -465

Net cash flow from / (used in) op. activities -2 761 -2 860

Cash flow from investing activities

Investment in fixed assets 6 -16

Investment in intangible assets -406 -

Investment in associated companies - -31

Investment in subsidiary (1) - -

Sale of subsidiary (1) - -

Net cash flow from / (used in) investing activities -400 -47

Cash flow from financing activities

Net proceeds from share issues 8 624 -

Proceeds from minority interest - -

Net cash flow from / (used in) finaning activities 8 624 0

Net inc / (dec) in cash and cash equivalents 5 462 -2 907

(1) Cash effects are net of cash received on sale of subsidiary,

and cash held by the subsidiary.

20

Agenda

Highlights

Operational review

Financial review

Technology update

21

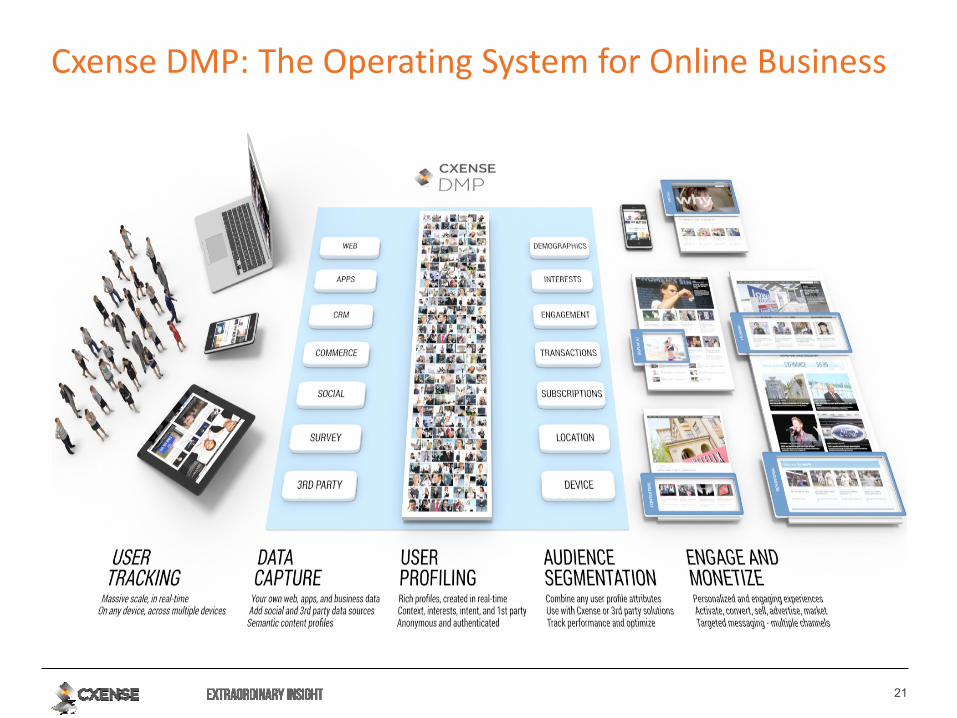

Cxense DMP: The Operating System for Online Business

22

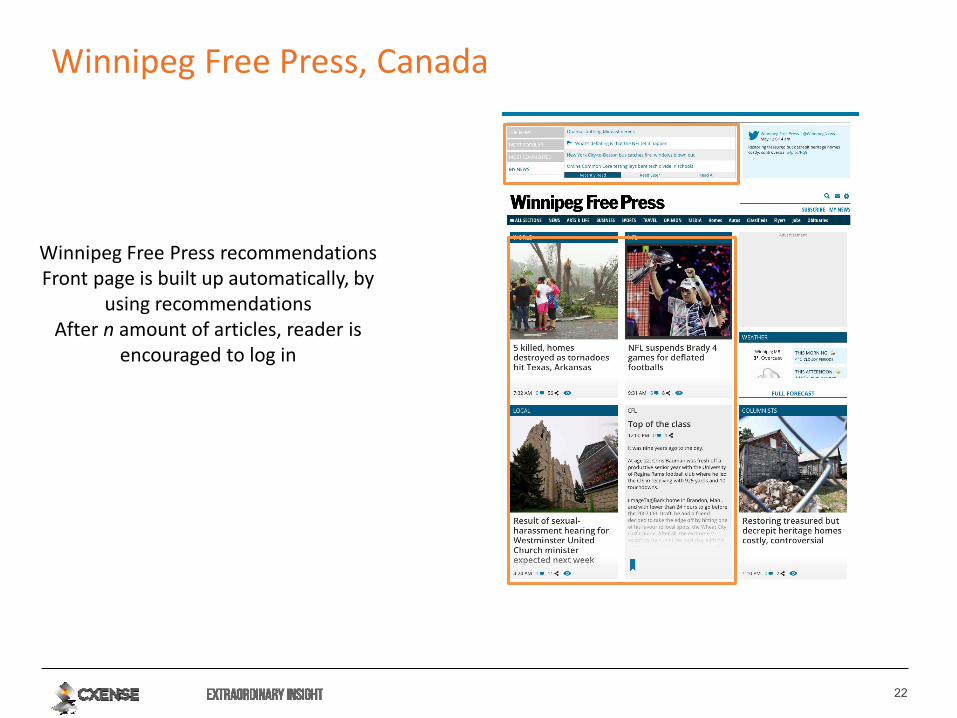

Winnipeg Free Press, Canada

Winnipeg Free Press recommendations Front page is built up automatically, by

using recommendations After n amount of articles, reader is

encouraged to log in

23

Excelsior, Mexico

Excelsior.com.mx,

topic pages and front-page Content

recommendation widgets automatically building topic pages

24

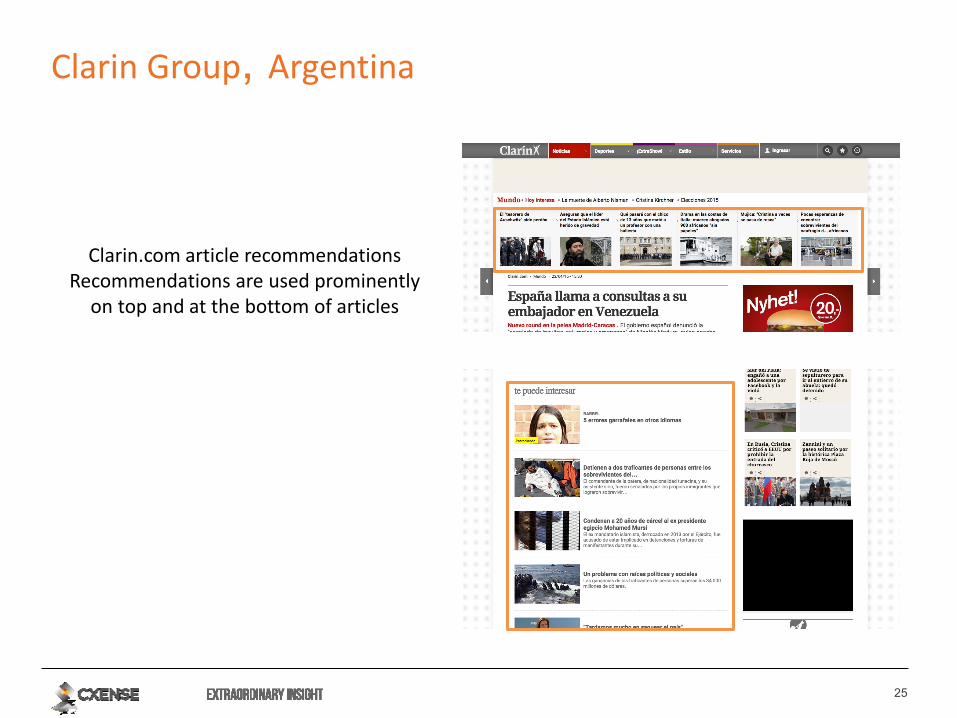

Clarin Group, Argentina

Clarin TyC Video recommendations

Usage of Cxense technology made CTR soar to 6% on recommendations

25

Clarin Group, Argentina

Clarin.com article recommendations Recommendations are used prominently

on top and at the bottom of articles

26

Summary Q1 2015

31 new contracts signed in the quarter

Record new recurring revenue

Cxense DMP is continuing to drive revenue growth

Higher churn from the acquired base, but expected to be back to normalized level in Q2 2015

Cost control and significant reduction in operating cost

Gross margin of 84%

Q&A Next event: Q2 2015 – 26 August 2015

28 12.05.2015

Customer case studies from around the globe – demos & workshops using Cxense tech Register today to attend: Cxense.com/CXXP

John Paton CEO

Digital First Media

Elsie Cheung COO

South China Morning Post

Achillefs Manolopoulos Head of Digital UX

Commercial Bank of Dubai