J. Lauritzen A/S 2013 H1 updatestatic.j-l.com/imce/Investorrelations/jl_-_h1_2013_update_(15... ·...

25

www.j-l.com | Oceans of know-how J. Lauritzen A/S 2013 H1 update August 2013

Transcript of J. Lauritzen A/S 2013 H1 updatestatic.j-l.com/imce/Investorrelations/jl_-_h1_2013_update_(15... ·...

www.j-l.com | Oceans of know-how

J. Lauritzen A/S

2013 H1 update

August 2013

Disclaimer

• This presentation contains forward-looking statements concerning J. Lauritzen A/S (“J. Lauritzen”, “JL” or the “Group”) and its financial condition, results of

operations and business. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking

statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown

risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements.

• Forward-looking statements include, among other things, statements concerning J. Lauritzen’s potential exposure to market risks and statements expressing

management’s expectations, beliefs, estimates, forecasts, projections and assumptions. There are numerous factors that could affect J. Lauritzen A/S’ future

operations and could cause J. Lauritzen A/S’ results to differ materially from those expressed in the forward-looking statements included in this presentation.

• All forward-looking statements contained in this presentation are expressly qualified by the cautionary statements contained or referenced to in this statement.

Undue reliance should not be placed on forward-looking statements.

• Each forward-looking statement speaks only as of the date of this presentation. J. Lauritzen does not undertake any obligation to publicly update or revise

any forward-looking statement as a result of new information or future events other than required by applicable law. In light of these risks, results could differ

materially from those stated, implied or inferred from the forward-looking statements contained in this presentation.

• Some of the statistical and graphical information contained in the presentation is supplied from the Clarkson Research Services Limited (“CRSL”) database

and other sources. CRSL has advised that (i) some information in CRSL’s database is derived from estimates or subjective judgments, (ii) the information in

the databases of other maritime data collection agencies may differ from the information in CRSL’s database, (iii) whilst CRSL has taken reasonable care in

the compilation of the statistical and graphical information and believes it to be accurate and correct, data compilation is subject to limited audit and validation

procedures and may accordingly contain errors, (iv) CRSL, its agents, officers and employees cannot accept liability for any loss suffered in consequence of

reliance on such information or in any other manner, and (v) the provision of such information does not obviate any need to make appropriate further

enquiries. Any use of such data and graphical information appear with reference to Clarkson Research Services Limited

• While the information in the presentation is believed to be accurate, no representation or warranty, express or implied, is or will be made in relation to the

accuracy or completeness of this presentation or any other written or oral information transmitted or made available to any person or its advisors in connection

with any investigation of the Group and no responsibility or liability is or will be accepted by the Group or any of their respective affiliates and representatives.

In particular, no representation or warranty, express or implied, is or will be given as to the achievement or reasonableness of any statements, estimates and

projections with respect to the anticipated future performance of the Group and the market for the Group’s products and services.

August 2013 2

www.j-l.com | Oceans of know-how

AGENDA

• First half of 2013

• Outlook for FY 2013

• Strategy update

• Financing

• Summary

3 August 2013

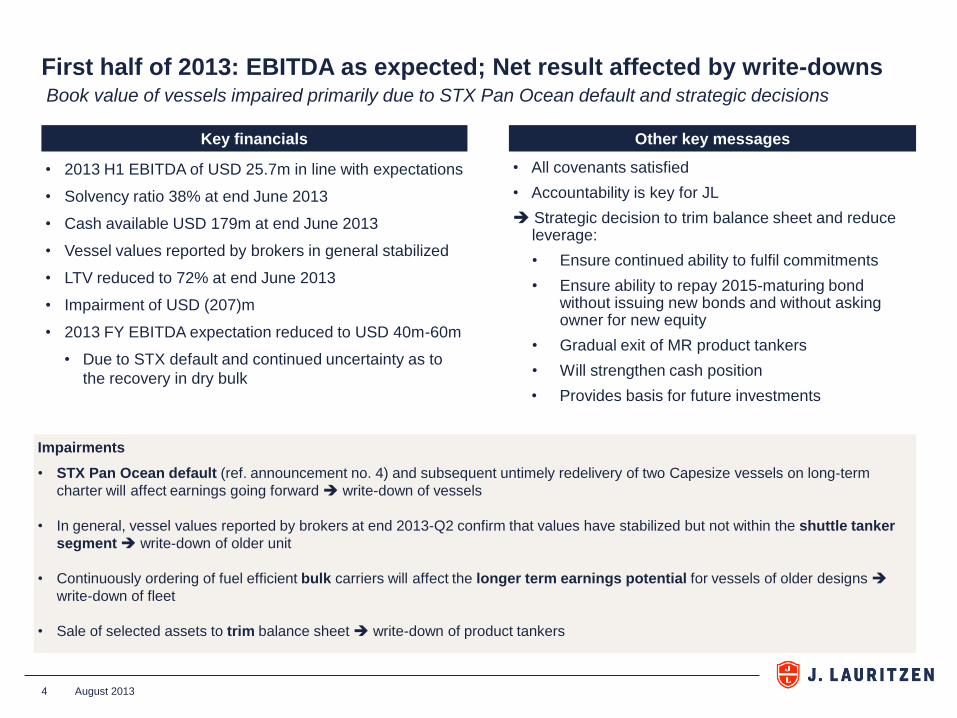

Impairments

• STX Pan Ocean default (ref. announcement no. 4) and subsequent untimely redelivery of two Capesize vessels on long-term

charter will affect earnings going forward write-down of vessels

• In general, vessel values reported by brokers at end 2013-Q2 confirm that values have stabilized but not within the shuttle tanker

segment write-down of older unit

• Continuously ordering of fuel efficient bulk carriers will affect the longer term earnings potential for vessels of older designs

write-down of fleet

• Sale of selected assets to trim balance sheet write-down of product tankers

August 2013 4

• All covenants satisfied

• Accountability is key for JL

Strategic decision to trim balance sheet and reduce leverage:

• Ensure continued ability to fulfil commitments

• Ensure ability to repay 2015-maturing bond without issuing new bonds and without asking owner for new equity

• Gradual exit of MR product tankers

• Will strengthen cash position

• Provides basis for future investments

Other key messages Key financials

• 2013 H1 EBITDA of USD 25.7m in line with expectations

• Solvency ratio 38% at end June 2013

• Cash available USD 179m at end June 2013

• Vessel values reported by brokers in general stabilized

• LTV reduced to 72% at end June 2013

• Impairment of USD (207)m

• 2013 FY EBITDA expectation reduced to USD 40m-60m

• Due to STX default and continued uncertainty as to

the recovery in dry bulk

First half of 2013: EBITDA as expected; Net result affected by write-downs Book value of vessels impaired primarily due to STX Pan Ocean default and strategic decisions

5

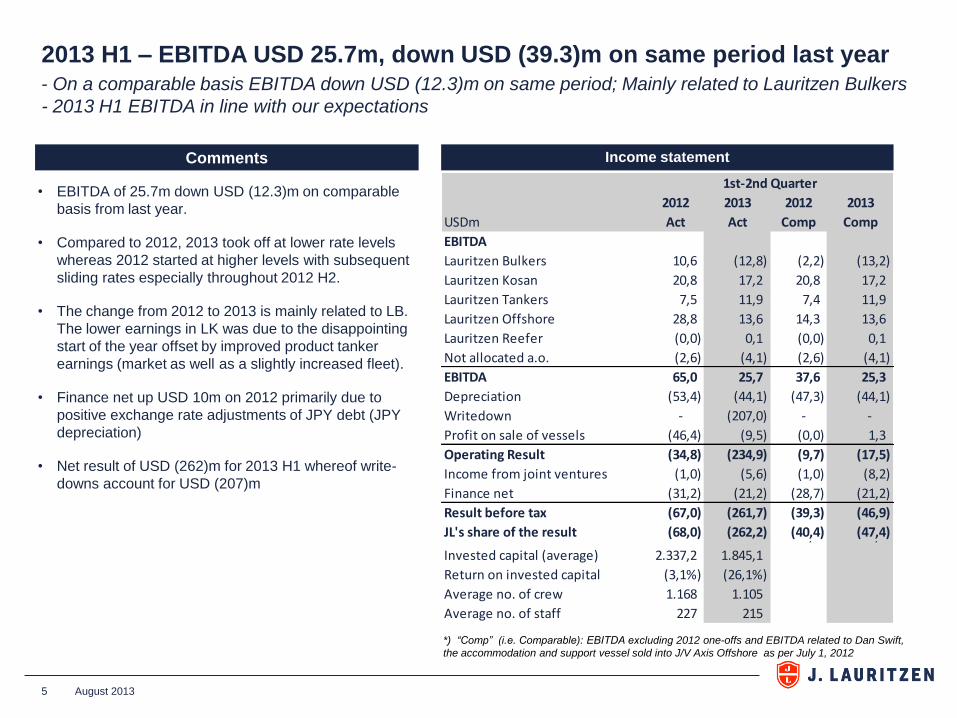

Income statement Comments

• EBITDA of 25.7m down USD (12.3)m on comparable

basis from last year.

• Compared to 2012, 2013 took off at lower rate levels

whereas 2012 started at higher levels with subsequent

sliding rates especially throughout 2012 H2.

• The change from 2012 to 2013 is mainly related to LB.

The lower earnings in LK was due to the disappointing

start of the year offset by improved product tanker

earnings (market as well as a slightly increased fleet).

• Finance net up USD 10m on 2012 primarily due to

positive exchange rate adjustments of JPY debt (JPY

depreciation)

• Net result of USD (262)m for 2013 H1 whereof write-

downs account for USD (207)m

August 2013

2013 H1 – EBITDA USD 25.7m, down USD (39.3)m on same period last year - On a comparable basis EBITDA down USD (12.3)m on same period; Mainly related to Lauritzen Bulkers

- 2013 H1 EBITDA in line with our expectations

2012 2013 2012 2013

USDm Act Act Comp Comp

EBITDA

Lauritzen Bulkers 10,6 (12,8) (2,2) (13,2)

Lauritzen Kosan 20,8 17,2 20,8 17,2

Lauritzen Tankers 7,5 11,9 7,4 11,9

Lauritzen Offshore 28,8 13,6 14,3 13,6

Lauritzen Reefer (0,0) 0,1 (0,0) 0,1

Not allocated a.o. (2,6) (4,1) (2,6) (4,1)

EBITDA 65,0 25,7 37,6 25,3

Depreciation (53,4) (44,1) (47,3) (44,1)

Writedown - (207,0) - -

Profit on sale of vessels (46,4) (9,5) (0,0) 1,3

Operating Result (34,8) (234,9) (9,7) (17,5)

Income from joint ventures (1,0) (5,6) (1,0) (8,2)

Finance net (31,2) (21,2) (28,7) (21,2)

Result before tax (67,0) (261,7) (39,3) (46,9)

JL's share of the result (68,0) (262,2) (40,4) (47,4)0,0 0,0

Invested capital (average) 2.337,2 1.845,1

Return on invested capital (3,1%) (26,1%)

Average no. of crew 1.168 1.105

Average no. of staff 227 215

1st-2nd Quarter

*) “Comp” (i.e. Comparable): EBITDA excluding 2012 one-offs and EBITDA related to Dan Swift,

the accommodation and support vessel sold into J/V Axis Offshore as per July 1, 2012

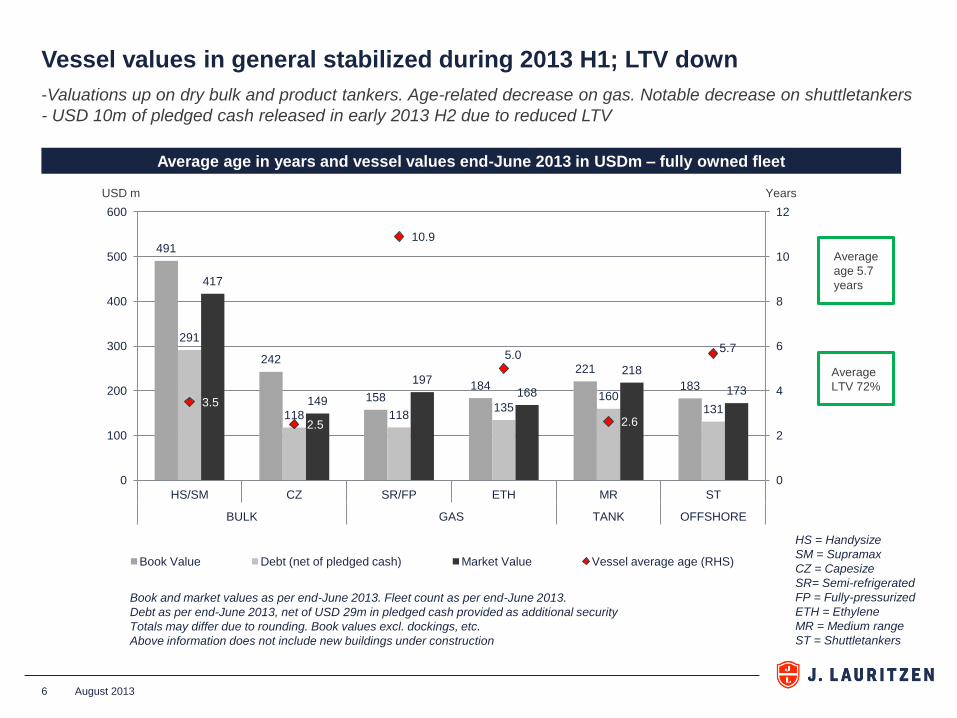

Vessel values in general stabilized during 2013 H1; LTV down

August 2013 6

-Valuations up on dry bulk and product tankers. Age-related decrease on gas. Notable decrease on shuttletankers

- USD 10m of pledged cash released in early 2013 H2 due to reduced LTV

Average age in years and vessel values end-June 2013 in USDm – fully owned fleet

491

242

158 184

221

183

291

118 118 135

160 131

417

149

197 168

218

173 3.5

2.5

10.9

5.0

2.6

5.7

0

2

4

6

8

10

12

0

100

200

300

400

500

600

HS/SM CZ SR/FP ETH MR ST

BULK GAS TANK OFFSHORE

Book Value Debt (net of pledged cash) Market Value Vessel average age (RHS)

USD m Years

Book and market values as per end-June 2013. Fleet count as per end-June 2013.

Debt as per end-June 2013, net of USD 29m in pledged cash provided as additional security

Totals may differ due to rounding. Book values excl. dockings, etc.

Above information does not include new buildings under construction

HS = Handysize

SM = Supramax

CZ = Capesize

SR= Semi-refrigerated

FP = Fully-pressurized

ETH = Ethylene

MR = Medium range

ST = Shuttletankers

Average

age 5.7

years

Average

LTV 72%

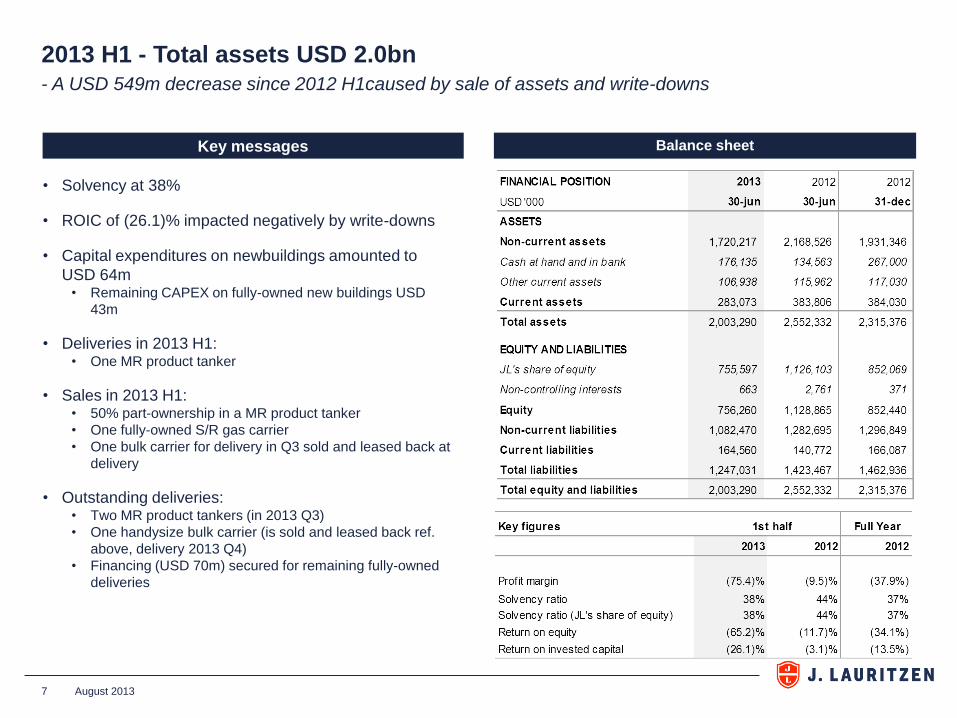

Balance sheet

7

Key messages

August 2013

2013 H1 - Total assets USD 2.0bn

- A USD 549m decrease since 2012 H1caused by sale of assets and write-downs

• Solvency at 38%

• ROIC of (26.1)% impacted negatively by write-downs

• Capital expenditures on newbuildings amounted to

USD 64m • Remaining CAPEX on fully-owned new buildings USD

43m

• Deliveries in 2013 H1: • One MR product tanker

• Sales in 2013 H1: • 50% part-ownership in a MR product tanker

• One fully-owned S/R gas carrier

• One bulk carrier for delivery in Q3 sold and leased back at

delivery

• Outstanding deliveries: • Two MR product tankers (in 2013 Q3)

• One handysize bulk carrier (is sold and leased back ref.

above, delivery 2013 Q4)

• Financing (USD 70m) secured for remaining fully-owned

deliveries

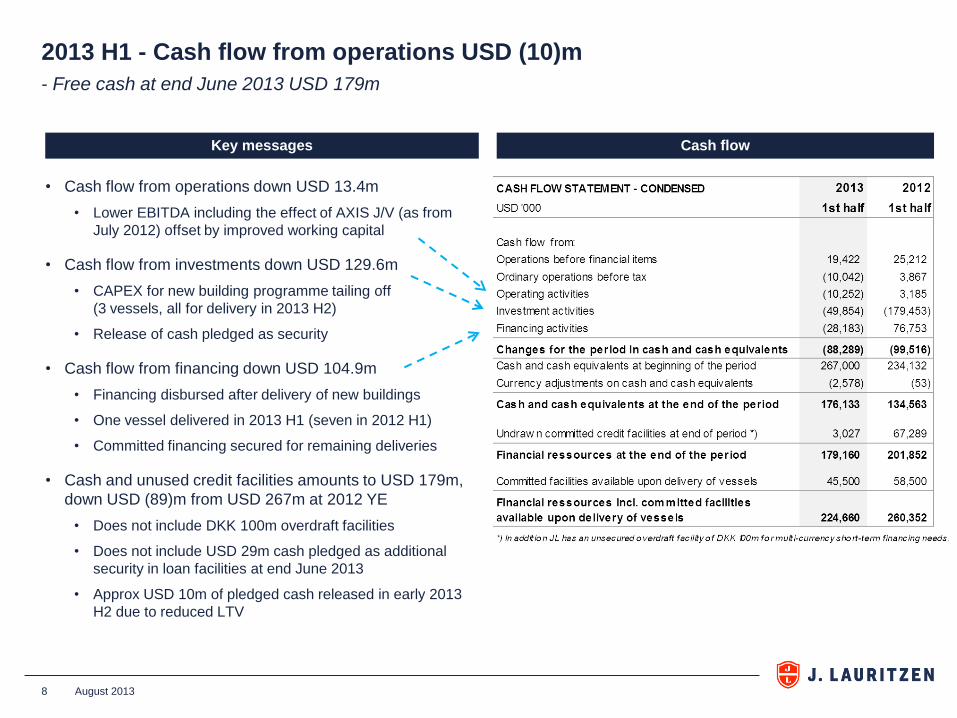

2013 H1 - Cash flow from operations USD (10)m

Cash flow

August 2013 8

Key messages

• Cash flow from operations down USD 13.4m

• Lower EBITDA including the effect of AXIS J/V (as from

July 2012) offset by improved working capital

• Cash flow from investments down USD 129.6m

• CAPEX for new building programme tailing off

(3 vessels, all for delivery in 2013 H2)

• Release of cash pledged as security

• Cash flow from financing down USD 104.9m

• Financing disbursed after delivery of new buildings

• One vessel delivered in 2013 H1 (seven in 2012 H1)

• Committed financing secured for remaining deliveries

• Cash and unused credit facilities amounts to USD 179m,

down USD (89)m from USD 267m at 2012 YE

• Does not include DKK 100m overdraft facilities

• Does not include USD 29m cash pledged as additional

security in loan facilities at end June 2013

• Approx USD 10m of pledged cash released in early 2013

H2 due to reduced LTV

- Free cash at end June 2013 USD 179m

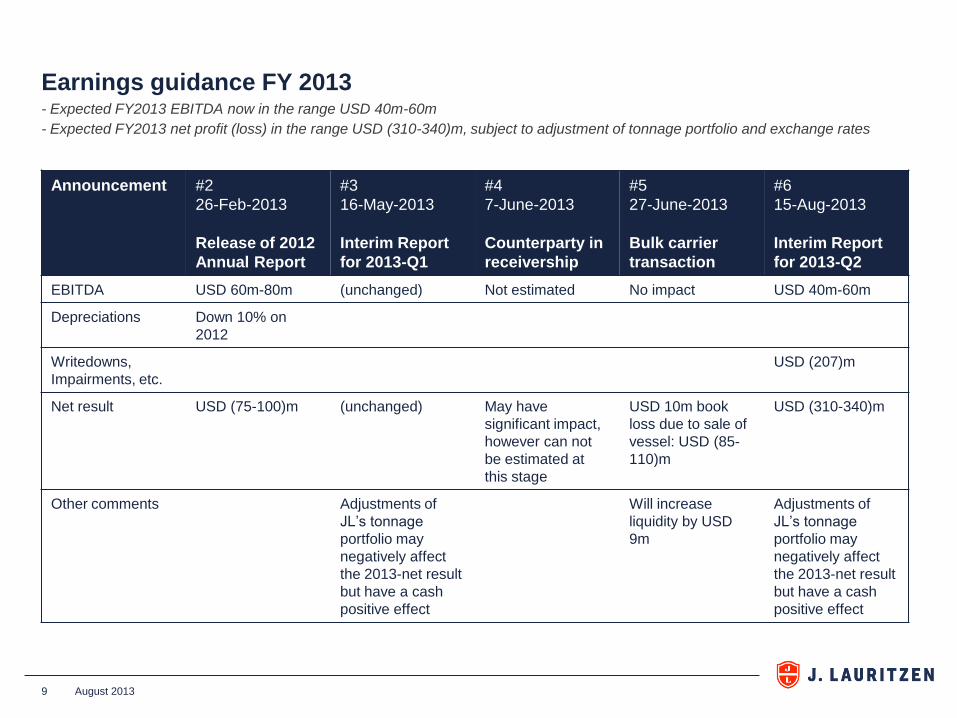

Earnings guidance FY 2013 - Expected FY2013 EBITDA now in the range USD 40m-60m

- Expected FY2013 net profit (loss) in the range USD (310-340)m, subject to adjustment of tonnage portfolio and exchange rates

9 August 2013

Announcement #2

26-Feb-2013

Release of 2012

Annual Report

#3

16-May-2013

Interim Report

for 2013-Q1

#4

7-June-2013

Counterparty in

receivership

#5

27-June-2013

Bulk carrier

transaction

#6

15-Aug-2013

Interim Report

for 2013-Q2

EBITDA USD 60m-80m (unchanged) Not estimated No impact USD 40m-60m

Depreciations Down 10% on

2012

Writedowns,

Impairments, etc.

USD (207)m

Net result USD (75-100)m (unchanged) May have

significant impact,

however can not

be estimated at

this stage

USD 10m book

loss due to sale of

vessel: USD (85-

110)m

USD (310-340)m

Other comments Adjustments of

JL’s tonnage

portfolio may

negatively affect

the 2013-net result

but have a cash

positive effect

Will increase

liquidity by USD

9m

Adjustments of

JL’s tonnage

portfolio may

negatively affect

the 2013-net result

but have a cash

positive effect

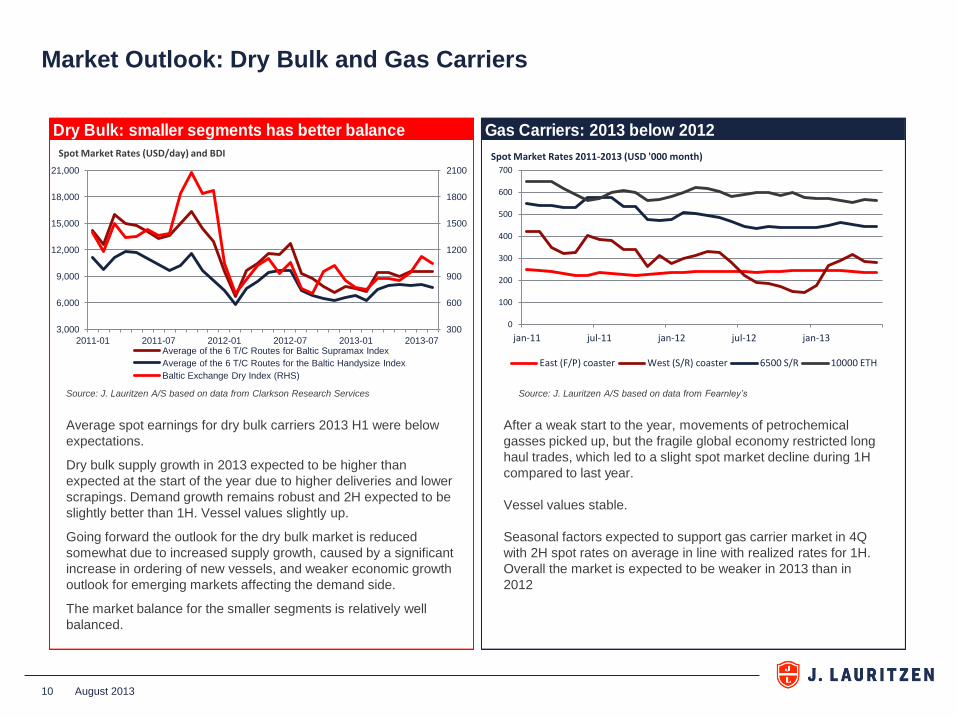

Dry Bulk: smaller segments has better balance Gas Carriers: 2013 below 2012

Average spot earnings for dry bulk carriers 2013 H1 were below

expectations.

Dry bulk supply growth in 2013 expected to be higher than

expected at the start of the year due to higher deliveries and lower

scrapings. Demand growth remains robust and 2H expected to be

slightly better than 1H. Vessel values slightly up.

Going forward the outlook for the dry bulk market is reduced

somewhat due to increased supply growth, caused by a significant

increase in ordering of new vessels, and weaker economic growth

outlook for emerging markets affecting the demand side.

The market balance for the smaller segments is relatively well

balanced.

After a weak start to the year, movements of petrochemical

gasses picked up, but the fragile global economy restricted long

haul trades, which led to a slight spot market decline during 1H

compared to last year.

Vessel values stable.

Seasonal factors expected to support gas carrier market in 4Q

with 2H spot rates on average in line with realized rates for 1H.

Overall the market is expected to be weaker in 2013 than in

2012

Source: J. Lauritzen A/S based on data from Clarkson Research Services Source: J. Lauritzen A/S based on data from Fearnley’s

10

Market Outlook: Dry Bulk and Gas Carriers

August 2013

300

600

900

1200

1500

1800

2100

3,000

6,000

9,000

12,000

15,000

18,000

21,000

2011-01 2011-07 2012-01 2012-07 2013-01 2013-07 Average of the 6 T/C Routes for Baltic Supramax Index

Average of the 6 T/C Routes for the Baltic Handysize Index

Baltic Exchange Dry Index (RHS)

Spot Market Rates (USD/day) and BDI

0

100

200

300

400

500

600

700

jan-11 jul-11 jan-12 jul-12 jan-13

Spot Market Rates 2011-2013 (USD '000 month)

East (F/P) coaster West (S/R) coaster 6500 S/R 10000 ETH

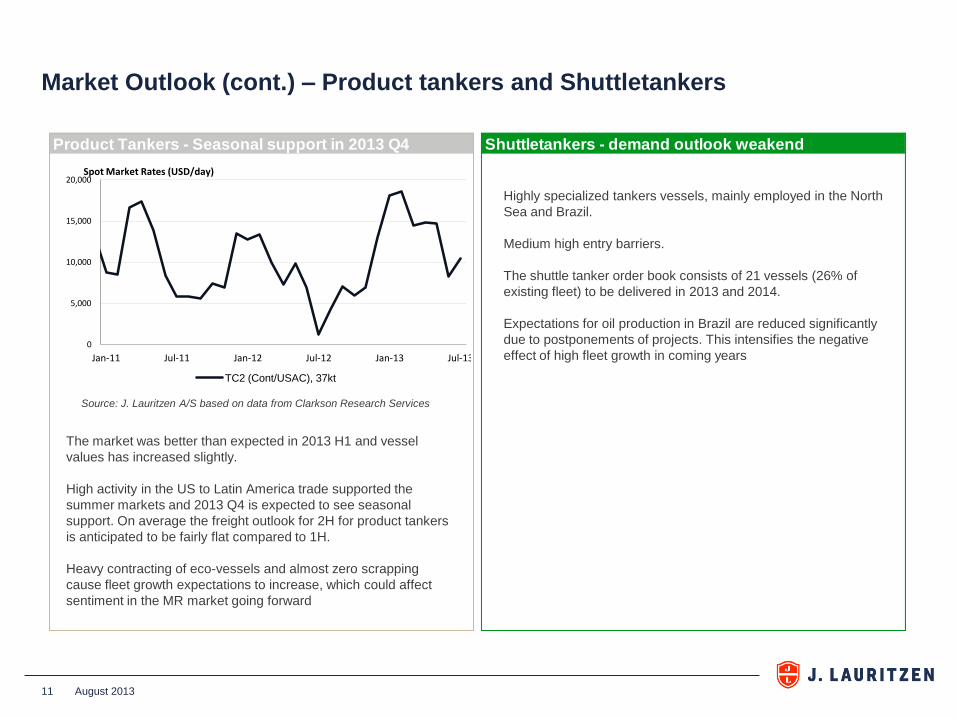

Product Tankers - Seasonal support in 2013 Q4 Shuttletankers - demand outlook weakend

11

The market was better than expected in 2013 H1 and vessel

values has increased slightly.

High activity in the US to Latin America trade supported the

summer markets and 2013 Q4 is expected to see seasonal

support. On average the freight outlook for 2H for product tankers

is anticipated to be fairly flat compared to 1H.

Heavy contracting of eco-vessels and almost zero scrapping

cause fleet growth expectations to increase, which could affect

sentiment in the MR market going forward

Highly specialized tankers vessels, mainly employed in the North

Sea and Brazil.

Medium high entry barriers.

The shuttle tanker order book consists of 21 vessels (26% of

existing fleet) to be delivered in 2013 and 2014.

Expectations for oil production in Brazil are reduced significantly

due to postponements of projects. This intensifies the negative

effect of high fleet growth in coming years

Source: J. Lauritzen A/S based on data from Clarkson Research Services

Market Outlook (cont.) – Product tankers and Shuttletankers

August 2013

0

5,000

10,000

15,000

20,000

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13

Spot Market Rates (USD/day)

TC2 (Cont/USAC), 37kt

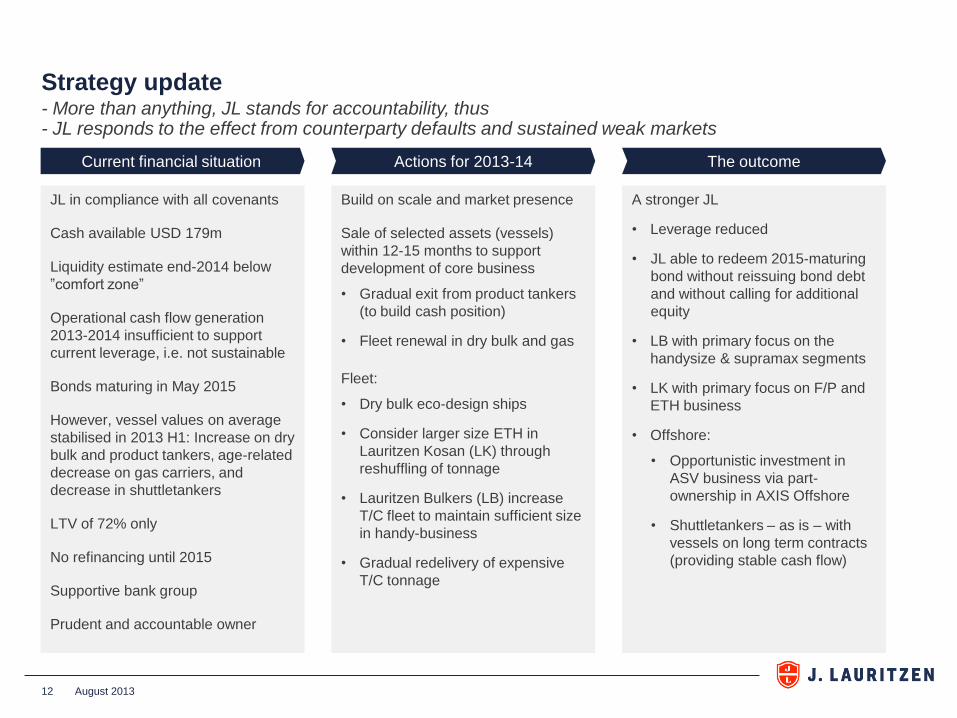

Strategy update - More than anything, JL stands for accountability, thus - JL responds to the effect from counterparty defaults and sustained weak markets

August 2013 12

Current financial situation

JL in compliance with all covenants

Cash available USD 179m

Liquidity estimate end-2014 below

”comfort zone”

Operational cash flow generation

2013-2014 insufficient to support

current leverage, i.e. not sustainable

Bonds maturing in May 2015

However, vessel values on average

stabilised in 2013 H1: Increase on dry

bulk and product tankers, age-related

decrease on gas carriers, and

decrease in shuttletankers

LTV of 72% only

No refinancing until 2015

Supportive bank group

Prudent and accountable owner

Actions for 2013-14

Build on scale and market presence

Sale of selected assets (vessels)

within 12-15 months to support

development of core business

• Gradual exit from product tankers

(to build cash position)

• Fleet renewal in dry bulk and gas

Fleet:

• Dry bulk eco-design ships

• Consider larger size ETH in

Lauritzen Kosan (LK) through

reshuffling of tonnage

• Lauritzen Bulkers (LB) increase

T/C fleet to maintain sufficient size

in handy-business

• Gradual redelivery of expensive

T/C tonnage

The outcome

A stronger JL

• Leverage reduced

• JL able to redeem 2015-maturing

bond without reissuing bond debt

and without calling for additional

equity

• LB with primary focus on the

handysize & supramax segments

• LK with primary focus on F/P and

ETH business

• Offshore:

• Opportunistic investment in

ASV business via part-

ownership in AXIS Offshore

• Shuttletankers – as is – with

vessels on long term contracts

(providing stable cash flow)

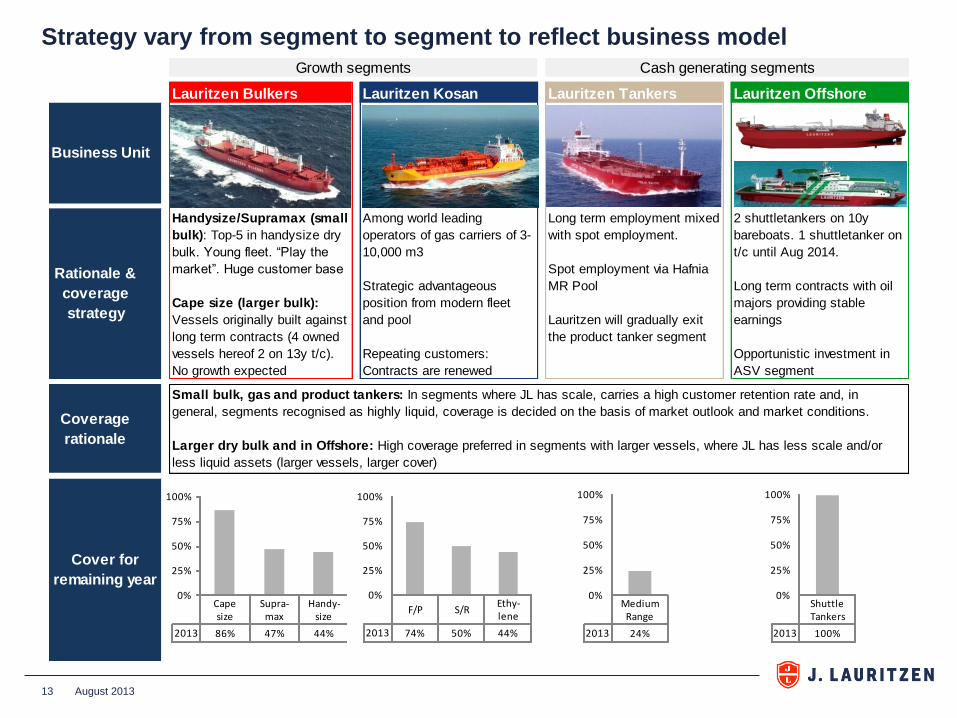

Strategy vary from segment to segment to reflect business model

August 2013 13

Lauritzen Bulkers Lauritzen Kosan Lauritzen Tankers Lauritzen Offshore

Growth segments Cash generating segments

Business Unit

Rationale &

coverage

strategy

Handysize/Supramax (small

bulk): Top-5 in handysize dry

bulk. Young fleet. “Play the

market”. Huge customer base

Cape size (larger bulk):

Vessels originally built against

long term contracts (4 owned

vessels hereof 2 on 13y t/c).

No growth expected

Among world leading

operators of gas carriers of 3-

10,000 m3

Strategic advantageous

position from modern fleet

and pool

Repeating customers:

Contracts are renewed

Long term employment mixed

with spot employment.

Spot employment via Hafnia

MR Pool

Lauritzen will gradually exit

the product tanker segment

2 shuttletankers on 10y

bareboats. 1 shuttletanker on

t/c until Aug 2014.

Long term contracts with oil

majors providing stable

earnings

Opportunistic investment in

ASV segment

Coverage

rationale

Small bulk, gas and product tankers: In segments where JL has scale, carries a high customer retention rate and, in

general, segments recognised as highly liquid, coverage is decided on the basis of market outlook and market conditions.

Larger dry bulk and in Offshore: High coverage preferred in segments with larger vessels, where JL has less scale and/or

less liquid assets (larger vessels, larger cover)

Cover for

remaining year

Cape size

Supra-max

Handy-size

2013 86% 47% 44%

0%

25%

50%

75%

100%

F/P S/REthy-lene

2013 74% 50% 44%

0%

25%

50%

75%

100%

Medium Range

2013 24%

0%

25%

50%

75%

100%

Shuttle Tankers

2013 100%

0%

25%

50%

75%

100%

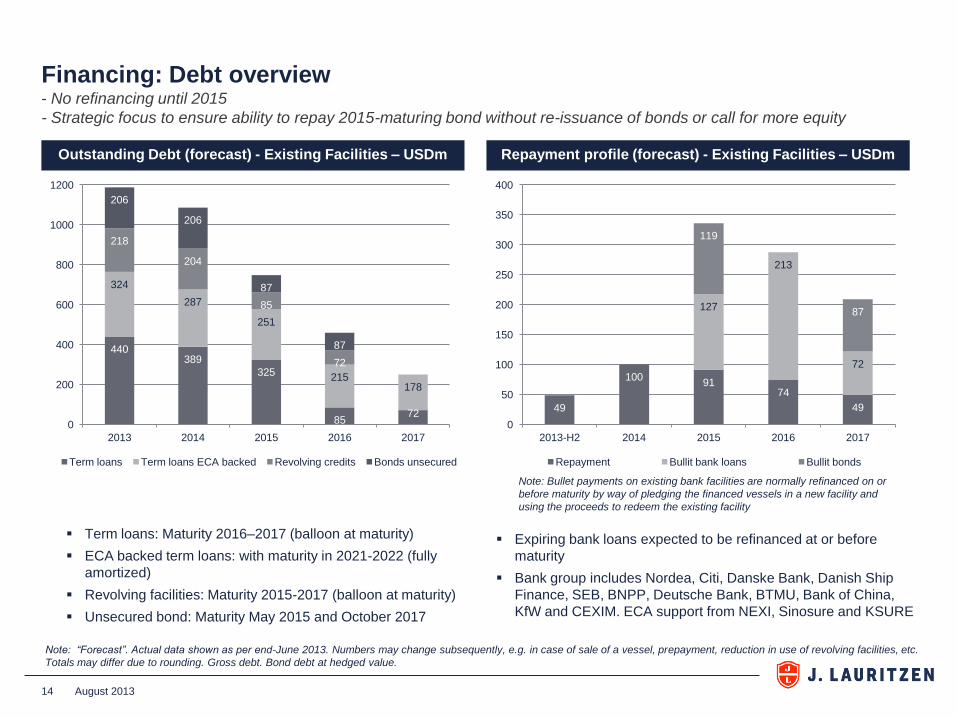

Financing: Debt overview - No refinancing until 2015

- Strategic focus to ensure ability to repay 2015-maturing bond without re-issuance of bonds or call for more equity

August 2013 14

Outstanding Debt (forecast) - Existing Facilities – USDm Repayment profile (forecast) - Existing Facilities – USDm

Expiring bank loans expected to be refinanced at or before

maturity

Bank group includes Nordea, Citi, Danske Bank, Danish Ship

Finance, SEB, BNPP, Deutsche Bank, BTMU, Bank of China,

KfW and CEXIM. ECA support from NEXI, Sinosure and KSURE

Term loans: Maturity 2016–2017 (balloon at maturity)

ECA backed term loans: with maturity in 2021-2022 (fully

amortized)

Revolving facilities: Maturity 2015-2017 (balloon at maturity)

Unsecured bond: Maturity May 2015 and October 2017

Note: Bullet payments on existing bank facilities are normally refinanced on or

before maturity by way of pledging the financed vessels in a new facility and

using the proceeds to redeem the existing facility

Note: “Forecast”. Actual data shown as per end-June 2013. Numbers may change subsequently, e.g. in case of sale of a vessel, prepayment, reduction in use of revolving facilities, etc.

Totals may differ due to rounding. Gross debt. Bond debt at hedged value.

49

100 91

74

49

127

213

72

119

87

0

50

100

150

200

250

300

350

400

2013-H2 2014 2015 2016 2017

Repayment Bullit bank loans Bullit bonds

440 389

325

85 72

324

287

251

215 178

218

204

85

72

206

206

87

87

0

200

400

600

800

1000

1200

2013 2014 2015 2016 2017

Term loans Term loans ECA backed Revolving credits Bonds unsecured

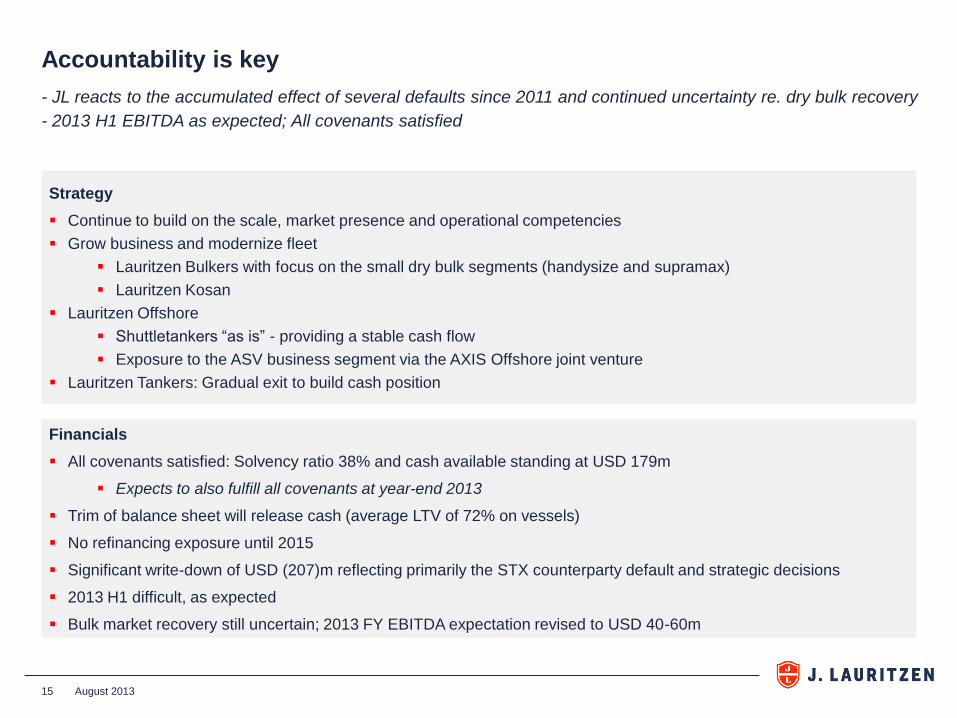

Accountability is key

August 2013 15

Financials

All covenants satisfied: Solvency ratio 38% and cash available standing at USD 179m

Expects to also fulfill all covenants at year-end 2013

Trim of balance sheet will release cash (average LTV of 72% on vessels)

No refinancing exposure until 2015

Significant write-down of USD (207)m reflecting primarily the STX counterparty default and strategic decisions

2013 H1 difficult, as expected

Bulk market recovery still uncertain; 2013 FY EBITDA expectation revised to USD 40-60m

Strategy

Continue to build on the scale, market presence and operational competencies

Grow business and modernize fleet

Lauritzen Bulkers with focus on the small dry bulk segments (handysize and supramax)

Lauritzen Kosan

Lauritzen Offshore

Shuttletankers “as is” - providing a stable cash flow

Exposure to the ASV business segment via the AXIS Offshore joint venture

Lauritzen Tankers: Gradual exit to build cash position

- JL reacts to the accumulated effect of several defaults since 2011 and continued uncertainty re. dry bulk recovery

- 2013 H1 EBITDA as expected; All covenants satisfied

www.j-l.com | Oceans of know-how

Appendix • Fleet overview

• Management

• Group Structure

• Ownership

• Lauritzen Fonden

• Glossary

• Contact details

• Vessel list

August 2013 16

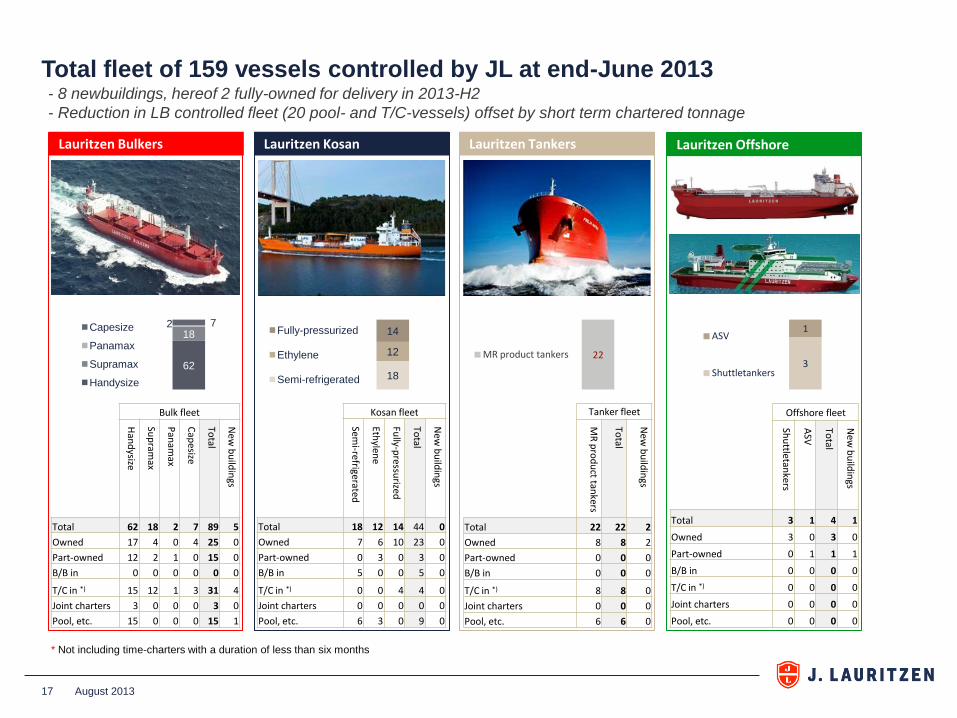

Total fleet of 159 vessels controlled by JL at end-June 2013

17

Lauritzen Bulkers Lauritzen Kosan Lauritzen Tankers Lauritzen Offshore

* Not including time-charters with a duration of less than six months

- 8 newbuildings, hereof 2 fully-owned for delivery in 2013-H2

- Reduction in LB controlled fleet (20 pool- and T/C-vessels) offset by short term chartered tonnage

Bulk fleet

Han

dysize

Sup

ramax

Pan

amax

Cap

esize

Total

New

bu

ildin

gs

Total 62 18 2 7 89 5

Owned 17 4 0 4 25 0

Part-owned 12 2 1 0 15 0

B/B in 0 0 0 0 0 0

T/C in *) 15 12 1 3 31 4

Joint charters 3 0 0 0 3 0

Pool, etc. 15 0 0 0 15 1

Kosan fleet

Semi-refrigerated

Ethylen

e

Fully-p

ressurized

Total

New

bu

ildin

gs Total 18 12 14 44 0

Owned 7 6 10 23 0

Part-owned 0 3 0 3 0

B/B in 5 0 0 5 0

T/C in *) 0 0 4 4 0

Joint charters 0 0 0 0 0

Pool, etc. 6 3 0 9 0

Offshore fleet

Shu

ttletankers

ASV

Total

New

bu

ildin

gs

Total 3 1 4 1

Owned 3 0 3 0

Part-owned 0 1 1 1

B/B in 0 0 0 0

T/C in *) 0 0 0 0

Joint charters 0 0 0 0

Pool, etc. 0 0 0 0

Tanker fleet

MR

pro

du

ct tankers

Total

New

bu

ildin

gs

Total 22 22 2

Owned 8 8 2

Part-owned 0 0 0

B/B in 0 0 0

T/C in *) 8 8 0

Joint charters 0 0 0

Pool, etc. 6 6 0

62

18 2 7 Capesize

Panamax

Supramax

Handysize 18

12

14 Fully-pressurized

Ethylene

Semi-refrigerated

22 MR product tankers 3

1 ASV

Shuttletankers

August 2013

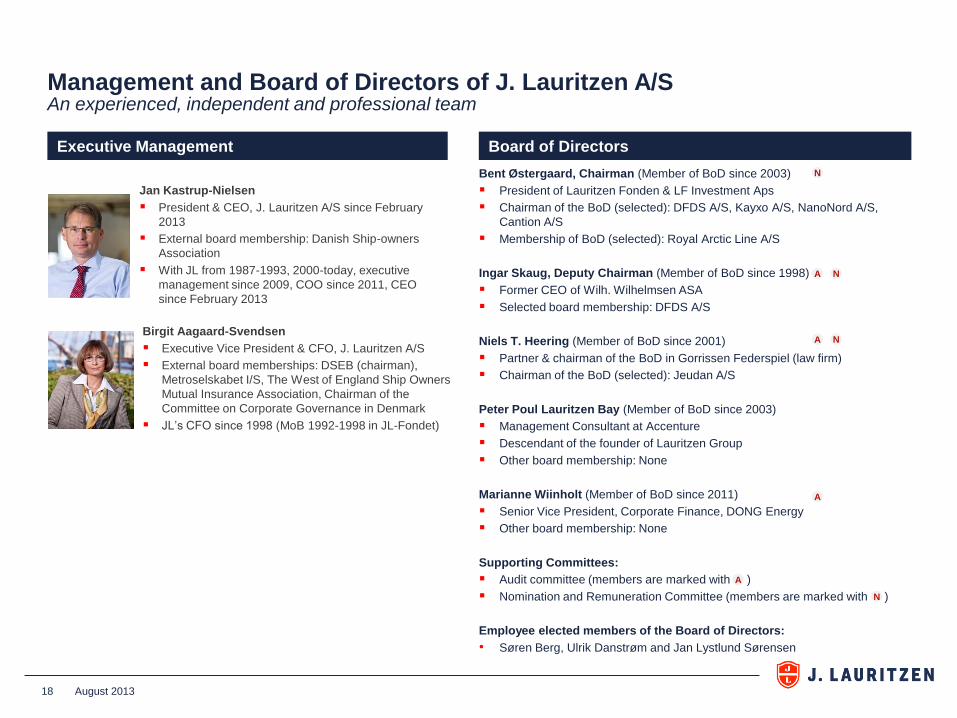

Bent Østergaard, Chairman (Member of BoD since 2003)

President of Lauritzen Fonden & LF Investment Aps

Chairman of the BoD (selected): DFDS A/S, Kayxo A/S, NanoNord A/S,

Cantion A/S

Membership of BoD (selected): Royal Arctic Line A/S

Ingar Skaug, Deputy Chairman (Member of BoD since 1998)

Former CEO of Wilh. Wilhelmsen ASA

Selected board membership: DFDS A/S

Niels T. Heering (Member of BoD since 2001)

Partner & chairman of the BoD in Gorrissen Federspiel (law firm)

Chairman of the BoD (selected): Jeudan A/S

Peter Poul Lauritzen Bay (Member of BoD since 2003)

Management Consultant at Accenture

Descendant of the founder of Lauritzen Group

Other board membership: None

Marianne Wiinholt (Member of BoD since 2011)

Senior Vice President, Corporate Finance, DONG Energy

Other board membership: None

Supporting Committees:

Audit committee (members are marked with )

Nomination and Remuneration Committee (members are marked with )

Employee elected members of the Board of Directors:

• Søren Berg, Ulrik Danstrøm and Jan Lystlund Sørensen

18

Executive Management Board of Directors

Birgit Aagaard-Svendsen

Executive Vice President & CFO, J. Lauritzen A/S

External board memberships: DSEB (chairman),

Metroselskabet I/S, The West of England Ship Owners

Mutual Insurance Association, Chairman of the

Committee on Corporate Governance in Denmark

JL’s CFO since 1998 (MoB 1992-1998 in JL-Fondet)

Jan Kastrup-Nielsen

President & CEO, J. Lauritzen A/S since February

2013

External board membership: Danish Ship-owners

Association

With JL from 1987-1993, 2000-today, executive

management since 2009, COO since 2011, CEO

since February 2013

N

N A

N A

A

A

N

August 2013

Management and Board of Directors of J. Lauritzen A/S An experienced, independent and professional team

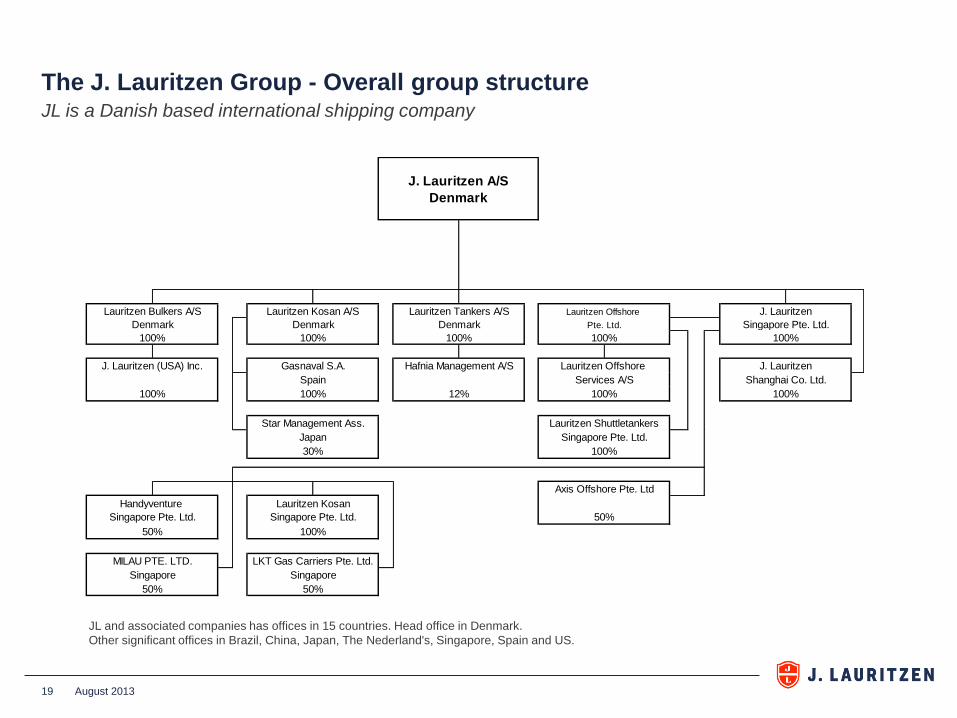

The J. Lauritzen Group - Overall group structure

August 2013 19

J. Lauritzen

Singapore Pte. Ltd.

100%

Axis Offshore Pte. Ltd

100%

100%

J. Lauritzen

Shanghai Co. Ltd.

100%100%

Services A/S

Singapore Pte. Ltd.

Lauritzen Shuttletankers

50%

Handyventure Lauritzen Kosan

Singapore Pte. Ltd. Singapore Pte. Ltd.

50% 100%

Lauritzen Bulkers A/S Lauritzen Tankers A/S

Denmark Denmark

Gasnaval S.A.

100% 100%

J. Lauritzen A/S

Denmark

Lauritzen Kosan A/S

Lauritzen Offshore

Denmark

100%

Lauritzen Offshore

Pte. Ltd.

50%

J. Lauritzen (USA) Inc. Hafnia Management A/S

LKT Gas Carriers Pte. Ltd.

Singapore

100%

Star Management Ass.

100% 12%

Japan

30%

MILAU PTE. LTD.

Singapore

50%

Spain

JL and associated companies has offices in 15 countries. Head office in Denmark.

Other significant offices in Brazil, China, Japan, The Nederland's, Singapore, Spain and US.

JL is a Danish based international shipping company

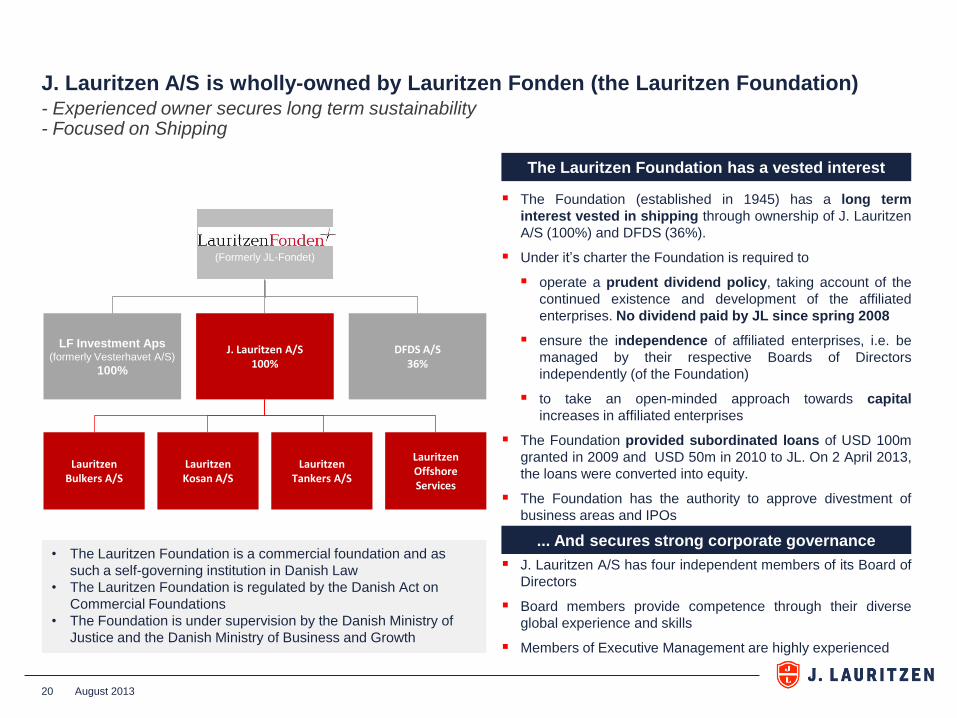

J. Lauritzen A/S is wholly-owned by Lauritzen Fonden (the Lauritzen Foundation) - Experienced owner secures long term sustainability - Focused on Shipping

20

LF Investment Aps (formerly Vesterhavet A/S)

100%

J. Lauritzen A/S 100%

DFDS A/S 36%

(Formerly JL-Fondet)

Lauritzen Bulkers A/S

Lauritzen Kosan A/S

Lauritzen Tankers A/S

Lauritzen Offshore Services

The Foundation (established in 1945) has a long term

interest vested in shipping through ownership of J. Lauritzen

A/S (100%) and DFDS (36%).

Under it’s charter the Foundation is required to

operate a prudent dividend policy, taking account of the

continued existence and development of the affiliated

enterprises. No dividend paid by JL since spring 2008

ensure the independence of affiliated enterprises, i.e. be

managed by their respective Boards of Directors

independently (of the Foundation)

to take an open-minded approach towards capital

increases in affiliated enterprises

The Foundation provided subordinated loans of USD 100m

granted in 2009 and USD 50m in 2010 to JL. On 2 April 2013,

the loans were converted into equity.

The Foundation has the authority to approve divestment of

business areas and IPOs

J. Lauritzen A/S has four independent members of its Board of

Directors

Board members provide competence through their diverse

global experience and skills

Members of Executive Management are highly experienced

The Lauritzen Foundation has a vested interest

... And secures strong corporate governance • The Lauritzen Foundation is a commercial foundation and as

such a self-governing institution in Danish Law

• The Lauritzen Foundation is regulated by the Danish Act on

Commercial Foundations

• The Foundation is under supervision by the Danish Ministry of

Justice and the Danish Ministry of Business and Growth

August 2013

Lauritzen Fonden was established in 1945 by the brothers Ivar and Knud Lauritzen and their sister Anna Lønbjerg-Holm. It was established in connection with the 50 years anniversary of Dampskibsselskabet “Vesterhavet”. Vesterhavet was founded by their father Ditlev Lauritzen in 1895.

Chairman Board of Directors; Jens Ditlev Lauritzen (great grandchild of the founder of J. Lauritzen)

The objectives of the Foundation are (e.g.):

To work for the prestige of Denmark by promoting and developing Danish shipping, especially international shipping, and Danish enterprises in general

To support studies and projects of a technical, commercial or other nature in shipping, trade and industry, agriculture and other sectors

To support the education/training of young people in Denmark and abroad

To work towards vessels, workshops and other workplaces, offices and housing operated by the companies, especially those associated with the Foundation, being healthy, bright and well-maintained and that they should be organised so as best to promote job satisfaction, and to provide support for the personnel and institutions working for such purposes, especially in the shipping sector

To provide support for institutions, associations and people who, all in all, look after the interests of the shipping sector and people employed therein, especially such institutions and associations set up by those in the Lauritzen Group or its companies, or have supported, have an interest in or been associated with, and possibly seek to associate them to other humanitarian institutions that are not self-supporting, and also to set up and operate humanitarian institutions that operate in line with the above

To provide support for institutions, associations and people who are working to encourage awareness and esteem of Danish cultural activities, especially including corporate culture, education/training, self-improvement and character training of the young, studies into disease prevention, especially prophylaxis

To provide support for institutions, associations and people who are working to promote Nordic and international relations, also of a purely humanitarian nature

To provide support for institutions, companies, associations and people whose aims and work the Board feels it is proper to support

To provide support for people who have done service in one of the Foundation’s or the Lauritzen Group companies and to such people’s successors

21

Read more about Lauritzen Fonden at http://www.lauritzenfonden.com

August 2013

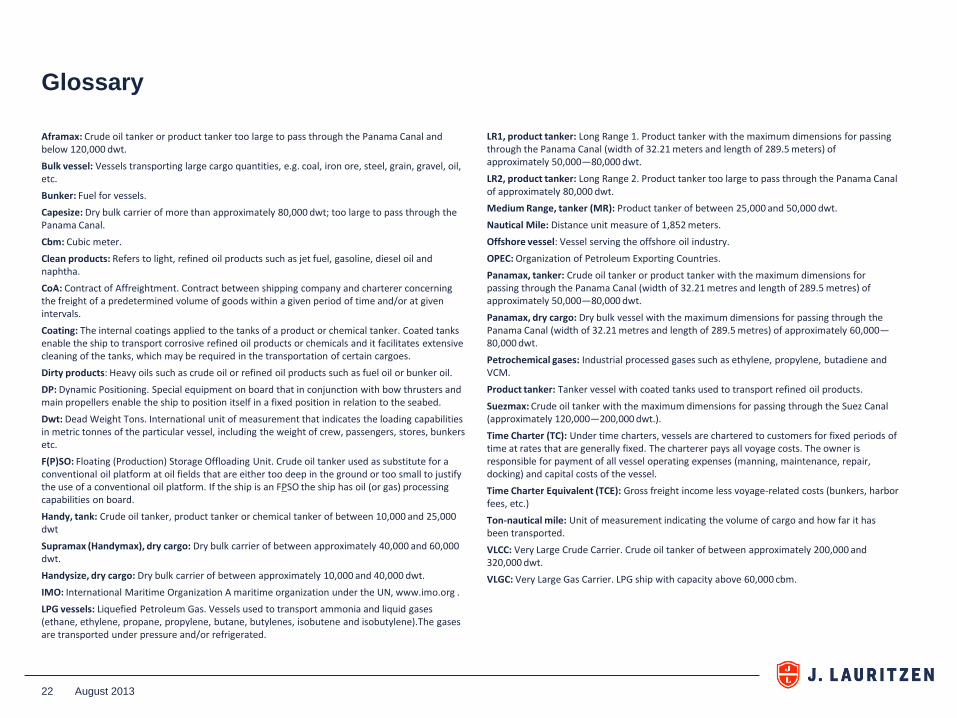

Glossary

Aframax: Crude oil tanker or product tanker too large to pass through the Panama Canal and below 120,000 dwt.

Bulk vessel: Vessels transporting large cargo quantities, e.g. coal, iron ore, steel, grain, gravel, oil, etc.

Bunker: Fuel for vessels.

Capesize: Dry bulk carrier of more than approximately 80,000 dwt; too large to pass through the Panama Canal.

Cbm: Cubic meter.

Clean products: Refers to light, refined oil products such as jet fuel, gasoline, diesel oil and naphtha.

CoA: Contract of Affreightment. Contract between shipping company and charterer concerning the freight of a predetermined volume of goods within a given period of time and/or at given intervals.

Coating: The internal coatings applied to the tanks of a product or chemical tanker. Coated tanks enable the ship to transport corrosive refined oil products or chemicals and it facilitates extensive cleaning of the tanks, which may be required in the transportation of certain cargoes.

Dirty products: Heavy oils such as crude oil or refined oil products such as fuel oil or bunker oil.

DP: Dynamic Positioning. Special equipment on board that in conjunction with bow thrusters and main propellers enable the ship to position itself in a fixed position in relation to the seabed.

Dwt: Dead Weight Tons. International unit of measurement that indicates the loading capabilities in metric tonnes of the particular vessel, including the weight of crew, passengers, stores, bunkers etc.

F(P)SO: Floating (Production) Storage Offloading Unit. Crude oil tanker used as substitute for a conventional oil platform at oil fields that are either too deep in the ground or too small to justify the use of a conventional oil platform. If the ship is an FPSO the ship has oil (or gas) processing capabilities on board.

Handy, tank: Crude oil tanker, product tanker or chemical tanker of between 10,000 and 25,000 dwt

Supramax (Handymax), dry cargo: Dry bulk carrier of between approximately 40,000 and 60,000 dwt.

Handysize, dry cargo: Dry bulk carrier of between approximately 10,000 and 40,000 dwt.

IMO: International Maritime Organization A maritime organization under the UN, www.imo.org .

LPG vessels: Liquefied Petroleum Gas. Vessels used to transport ammonia and liquid gases (ethane, ethylene, propane, propylene, butane, butylenes, isobutene and isobutylene).The gases are transported under pressure and/or refrigerated.

LR1, product tanker: Long Range 1. Product tanker with the maximum dimensions for passing through the Panama Canal (width of 32.21 meters and length of 289.5 meters) of approximately 50,000—80,000 dwt.

LR2, product tanker: Long Range 2. Product tanker too large to pass through the Panama Canal of approximately 80,000 dwt.

Medium Range, tanker (MR): Product tanker of between 25,000 and 50,000 dwt.

Nautical Mile: Distance unit measure of 1,852 meters.

Offshore vessel: Vessel serving the offshore oil industry.

OPEC: Organization of Petroleum Exporting Countries.

Panamax, tanker: Crude oil tanker or product tanker with the maximum dimensions for passing through the Panama Canal (width of 32.21 metres and length of 289.5 metres) of approximately 50,000—80,000 dwt.

Panamax, dry cargo: Dry bulk vessel with the maximum dimensions for passing through the Panama Canal (width of 32.21 metres and length of 289.5 metres) of approximately 60,000—80,000 dwt.

Petrochemical gases: Industrial processed gases such as ethylene, propylene, butadiene and VCM.

Product tanker: Tanker vessel with coated tanks used to transport refined oil products.

Suezmax: Crude oil tanker with the maximum dimensions for passing through the Suez Canal (approximately 120,000—200,000 dwt.).

Time Charter (TC): Under time charters, vessels are chartered to customers for fixed periods of time at rates that are generally fixed. The charterer pays all voyage costs. The owner is responsible for payment of all vessel operating expenses (manning, maintenance, repair, docking) and capital costs of the vessel.

Time Charter Equivalent (TCE): Gross freight income less voyage-related costs (bunkers, harbor fees, etc.)

Ton-nautical mile: Unit of measurement indicating the volume of cargo and how far it has been transported.

VLCC: Very Large Crude Carrier. Crude oil tanker of between approximately 200,000 and 320,000 dwt.

VLGC: Very Large Gas Carrier. LPG ship with capacity above 60,000 cbm.

August 2013 22

Contact details

Investor relations

Jacob Winthereik Financial Investor Relationship Manager, Group Treasury

E-mail: [email protected]

Phone: +45 3396 8384

Web: http://www.j-l.com

Press & Media

Jens Søndergaard Senior Vice President,

Strategic Planning & Executive Communications

E-mail: [email protected]

Phone: +45 3396 8401

Web: http://www.j-l.com

August 2013 23

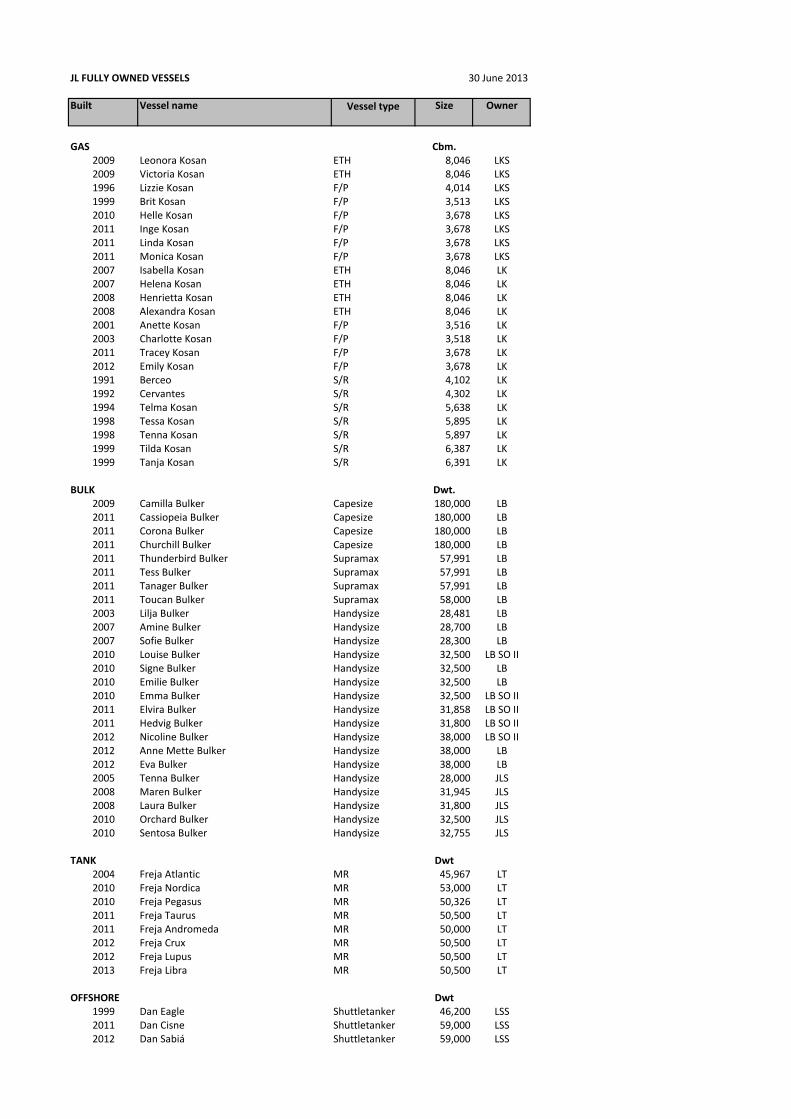

JL FULLY OWNED VESSELS 30 June 2013

Built Vessel name Size Owner

GAS Cbm.2009 Leonora Kosan ETH 8,046 LKS2009 Victoria Kosan ETH 8,046 LKS1996 Lizzie Kosan F/P 4,014 LKS1999 Brit Kosan F/P 3,513 LKS2010 Helle Kosan F/P 3,678 LKS2011 Inge Kosan F/P 3,678 LKS2011 Linda Kosan F/P 3,678 LKS2011 Monica Kosan F/P 3,678 LKS2007 Isabella Kosan ETH 8,046 LK2007 Helena Kosan ETH 8,046 LK2008 Henrietta Kosan ETH 8,046 LK2008 Alexandra Kosan ETH 8,046 LK2001 Anette Kosan F/P 3,516 LK2003 Charlotte Kosan F/P 3,518 LK2011 Tracey Kosan F/P 3,678 LK2012 Emily Kosan F/P 3,678 LK1991 Berceo S/R 4,102 LK1992 Cervantes S/R 4,302 LK1994 Telma Kosan S/R 5,638 LK1998 Tessa Kosan S/R 5,895 LK1998 Tenna Kosan S/R 5,897 LK1999 Tilda Kosan S/R 6,387 LK1999 Tanja Kosan S/R 6,391 LK

BULK Dwt.2009 Camilla Bulker Capesize 180,000 LB2011 Cassiopeia Bulker Capesize 180,000 LB2011 Corona Bulker Capesize 180,000 LB2011 Churchill Bulker Capesize 180,000 LB2011 Thunderbird Bulker Supramax 57,991 LB2011 Tess Bulker Supramax 57,991 LB2011 Tanager Bulker Supramax 57,991 LB2011 Toucan Bulker Supramax 58,000 LB2003 Lilja Bulker Handysize 28,481 LB2007 Amine Bulker Handysize 28,700 LB2007 Sofie Bulker Handysize 28,300 LB2010 Louise Bulker Handysize 32,500 LB SO II2010 Signe Bulker Handysize 32,500 LB2010 Emilie Bulker Handysize 32,500 LB2010 Emma Bulker Handysize 32,500 LB SO II2011 Elvira Bulker Handysize 31,858 LB SO II2011 Hedvig Bulker Handysize 31,800 LB SO II2012 Nicoline Bulker Handysize 38,000 LB SO II2012 Anne Mette Bulker Handysize 38,000 LB2012 Eva Bulker Handysize 38,000 LB2005 Tenna Bulker Handysize 28,000 JLS2008 Maren Bulker Handysize 31,945 JLS2008 Laura Bulker Handysize 31,800 JLS2010 Orchard Bulker Handysize 32,500 JLS2010 Sentosa Bulker Handysize 32,755 JLS

TANK Dwt2004 Freja Atlantic MR 45,967 LT2010 Freja Nordica MR 53,000 LT2010 Freja Pegasus MR 50,326 LT2011 Freja Taurus MR 50,500 LT2011 Freja Andromeda MR 50,000 LT2012 Freja Crux MR 50,500 LT2012 Freja Lupus MR 50,500 LT2013 Freja Libra MR 50,500 LT

OFFSHORE Dwt1999 Dan Eagle Shuttletanker 46,200 LSS2011 Dan Cisne Shuttletanker 59,000 LSS2012 Dan Sabiá Shuttletanker 59,000 LSS

Vessel type

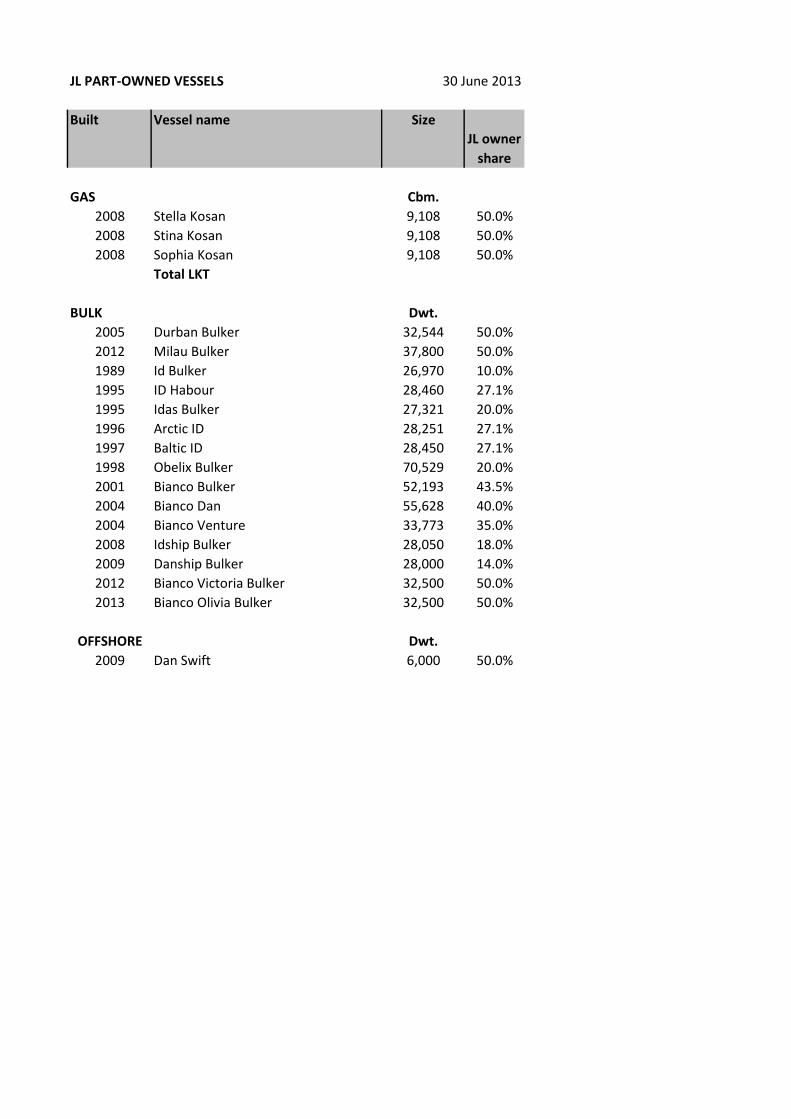

JL PART-OWNED VESSELS 30 June 2013

Built Vessel name Size

JL owner

share

GAS Cbm.

2008 Stella Kosan 9,108 50.0%

2008 Stina Kosan 9,108 50.0%

2008 Sophia Kosan 9,108 50.0%

Total LKT

BULK Dwt.

2005 Durban Bulker 32,544 50.0%

2012 Milau Bulker 37,800 50.0%

1989 Id Bulker 26,970 10.0%

1995 ID Habour 28,460 27.1%

1995 Idas Bulker 27,321 20.0%

1996 Arctic ID 28,251 27.1%

1997 Baltic ID 28,450 27.1%

1998 Obelix Bulker 70,529 20.0%

2001 Bianco Bulker 52,193 43.5%

2004 Bianco Dan 55,628 40.0%

2004 Bianco Venture 33,773 35.0%

2008 Idship Bulker 28,050 18.0%

2009 Danship Bulker 28,000 14.0%

2012 Bianco Victoria Bulker 32,500 50.0%

2013 Bianco Olivia Bulker 32,500 50.0%

OFFSHORE Dwt.

2009 Dan Swift 6,000 50.0%